Bitcoin Mining Squeeze: Who's Unprofitable, How Miners Respond, and Risks to BTC Liquidity

Summary

Executive snapshot

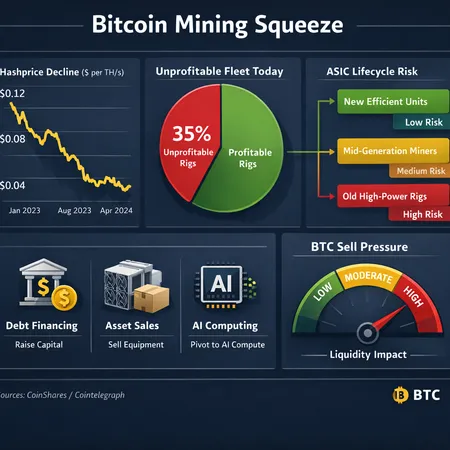

The mining sector is under pressure. CoinShares’ analysis — summarized by Cointelegraph and followed up by coverage at crypto.news — estimates that up to roughly 20% of the Bitcoin mining fleet may already be unprofitable at today’s hashprices. That number matters: miners are not an ideological supply bucket; they are operational businesses that can and will sell BTC or machines to stay liquid. For institutional allocators and macro analysts, the question is not only how many rigs are underwater today but how miners’ strategic responses could translate into BTC sell-pressure and market volatility.

What “unprofitable” means and how CoinShares reached ~20%

- Hashprice (USD earned per TH/day) is the primary short-term revenue metric for miners. When hashprice falls below the breakeven threshold implied by electricity, capex amortization and operational expenses, a rig or operation becomes technically unprofitable.

- CoinShares’ work — reported in Cointelegraph and in a follow-up by crypto.news — uses market BTC prices, network difficulty and industry cost estimates to identify the marginal fleet that is losing money. The headline: up to ~20% of the fleet sits at or below breakeven at recent hashprices (Cointelegraph summary; crypto.news follow-up).

- That 20% is a cross-section: older ASICs, high power costs, unfavorable electricity contracts and poor operational efficiency cluster in that segment.

Which miners are most at risk

Technical risk: ASIC lifecycle and efficiency

- Legacy rigs (end-of-life or older ASICs): Older-generation machines with low energy efficiency (high J/TH) have the highest breakeven hashprice. These rigs often have been paid for but are very sensitive to hashprice drops because their marginal operating costs (electricity) dominate.

- Mid-life rigs: Operators with mid-efficiency machines are vulnerable if they face higher-than-average power costs or limited access to capital for upgrades.

- Modern fleet: The newest, most efficient machines have the biggest cushion; many can remain profitable at lower hashprices.

Cost and operational risk

- High electricity-cost operations: Mines in jurisdictions with expensive tariffs or constrained grid access are near the margin even with modern hardware.

- Small/independent miners: Smaller operations often lack hedges, line-of-credit access, or inventory of BTC — so a short revenue shock forces immediate liquidity measures.

- Geographic concentration and regulatory risk: Local regulatory shifts (curtailments, taxes, permitting) can push otherwise intact operators into selling.

How miners are responding (evidence and implications)

Three trends stand out, backed by industry reporting:

Debt financing and leverage

- Miners are raising debt to bridge liquidity gaps or to finance new capex. Cryptoslate documented miners taking on debt while simultaneously selling BTC to maintain liquidity (Cryptoslate report).

- Debt helps short-term survival but introduces maturity and covenant risk: if BTC falls, lenders may demand additional collateral or accelerate repayment, forcing further asset sales.

BTC sales and inventory draws

- The obvious lever: sell mined BTC to cover operating costs. Many public miners report weekly/monthly sales; privately, distressed sellers can accelerate disposals, especially when debt covenants bind.

Asset sales, shutdowns and pivot strategies

- Operators will retire or sell older rigs (secondary market) when running them is uneconomic.

- Some large, well-capitalized miners are exploring AI compute pivoting (or hybrid operations) to monetize data-center assets when pure mining margins compress — a trend covered by Cryptoslate showing miners funding AI pivots with debt.

Translating the CoinShares figures into actionable scenarios

Below are illustrative scenarios using the CoinShares baseline (~20% unprofitable today). These are not predictions but stress-test frames you can use in portfolio models.

| Scenario | Hashprice move (relative) | Estimated unprofitable fleet | Market implication for BTC supply |

|---|---|---|---|

| Baseline (CoinShares) | 0% | ~20% | Ongoing, managed sales by margin operators; limited systemic stress |

| Mild shock | −10% | ~35% | Noticeable increase in miner sell-pressure as marginal units liquidate and some debt covenants are tested |

| Moderate shock | −25% | ~55% | Majority of legacy rigs unprofitable; accelerated selling, machine fire-sales, and debt restructurings likely |

| Severe shock | −40% | >70% | Broad distress across miner balance sheets; forced asset and BTC sales; risk of contagion to broader crypto funding markets |

Notes on the table: the sensitivity numbers are illustrative and intentionally conservative in their ramp; the real-world response curve depends on miner cash buffers, hedge positions, debt maturities and access to non-BTC liquidity.

Simple rig-class profitability example (stylized)

- Legacy rigs: breakeven hashprice = relatively high; a 10% hashprice drop flips many to loss.

- Mid-life rigs: breakeven is mid-range; survive moderate drops but suffer under prolonged compression.

- Modern rigs: lowest breakeven; can still be cash-positive through mild-moderate hashprice contractions.

This classification helps investors prioritize which miners to watch: those with high legacy exposure and tight liquidity are earliest forced sellers.

Systemic risk pathways to BTC liquidity and price

Direct sell-pressure: miners monetizing inventory represent a steady source of supply. If weekly miner sell volumes spike, they can overwhelm demand and depress the spot price.

Leverage and margin amplification: miners using debt create a feedback loop. Falling BTC → margin calls → forced sales → lower BTC price → more margin calls. Cryptoslate’s reporting shows miners are already leveraging to fund pivots and operations, increasing this vulnerability.

Machine fire-sales and second-order effects: widespread equipment liquidations reduce miners’ future capacity (lower hashrate growth), but short-term the sale of machines can depress secondary market values and impair collateral valuations for lenders.

Funding market contagion: if miner distress causes losses at lenders or prime brokers, credit tightening may spread to other crypto-native businesses and market makers, reducing market liquidity and widening bid-ask spreads.

Monitoring and indicators for institutional investors

Key data points and signals to track weekly or monthly:

- Miner BTC reserves vs. weekly production: how many weeks of BTC payroll/sales are left if mining revenues decline.

- Public miner balance-sheet metrics: debt outstanding, maturities, interest rates and covenant triggers.

- Hashprice and difficulty trajectory: watch hashprice across different difficulty-adjusted windows; falling hashprice combined with static/increasing difficulty is dangerous.

- Secondary market ASIC prices: falling resale values are an early sign of upcoming capex retrenchment and forced sales.

- Exchange inflows from miner-associated wallets: on-chain monitoring of known miner wallets depositing to exchanges can indicate impending sell-pressure.

- Concentration of hashrate: big players going distressed can have outsized effects.

For many allocators, platforms like Bitlet.app provide alternative liquidity channels and data that can augment your miner-flow models; use them alongside on-chain and industry reports.

Practical hedges and risk-management actions

- Stress-test allocations with miner-sell scenarios: incorporate miner supply shocks into your VaR and liquidity stress tests (use the scenario table above as one input).

- Trade execution readiness: widen your liquidity universe—use OTC desks and staggered execution plans to absorb miner flows without moving the market.

- Credit and counterparty diligence: underwrite exposure to miners and lenders aggressively; prioritize counterparties with conservative lending standards and strong collateralization.

- Derivatives hedges: options and futures can protect against sharp spot drops; consider collar strategies if miners’ liquidation risk is likely to cluster near known debt maturities.

What to watch next (90-day horizon)

- Public miner quarterly reports for disclosed BTC sales and debt issuance.

- On-chain flows from known mining pools and wallets to exchanges.

- Secondary ASIC pricing and liquidation announcements.

- Debt-market signals: rising yields on miner debt or distressed paper sales.

Final takeaways for investors

- CoinShares’ ~20% unprofitable estimate is a useful baseline — but it’s the slope, not the intercept, that matters. A modest hashprice decline can materially increase the proportion of the fleet that is marginal, and miners often respond by selling BTC or taking on risky leverage.

- The most vulnerable operators are those with legacy hardware, high power costs, concentrated geography, thin liquidity buffers and heavy near-term debt maturities.

- Systemic risk is non-linear: small spikes in miner selling can be absorbed, but leveraged mines and tight funding markets can convert a shock into amplified volatility.

- Institutional investors should build miner-driven supply scenarios into their liquidity and tail-risk planning, track miner balance sheets and wallet flows, and keep execution plans ready for periods of elevated sell-pressure.

For a deeper dive into miner liquidity strategies and tactical hedges, monitor industry reporting and weekly on-chain data; reputable outlets and research (for example the Cointelegraph summary of CoinShares and Cryptoslate coverage) remain invaluable inputs to any model.

Sources

- Cointelegraph — Bitcoin mining squeeze narrows field of viable operators (CoinShares summary)

- Cryptoslate — Bitcoin miners start funding pivot to AI with debt while selling BTC to stay liquid

- crypto.news — CoinShares says part of Bitcoin fleet is unprofitable

Internal reference: For context on network-level price signals and market narratives, traders frequently watch Bitcoin flows and related liquidity metrics, and sometimes juxtapose mining dynamics with activity on DeFi platforms when assessing derivative demand.