How Michael Saylor’s Corporate-Buying Strategy Reshaped Institutional Bitcoin Demand

Summary

Executive overview

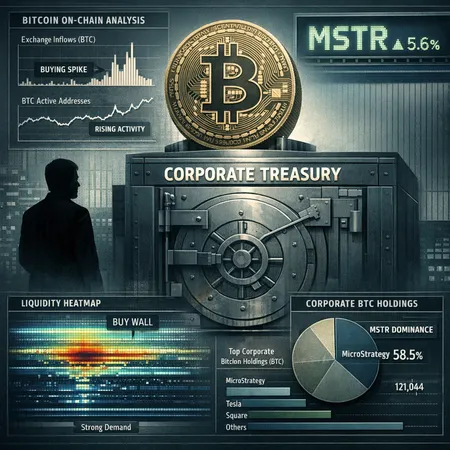

Michael Saylor’s high-conviction corporate Bitcoin strategy has stopped being a curiosity and become a macro force. Recent data analysis — reported via CryptoQuant and summarized in market coverage — shows that purchases linked to MicroStrategy (MSTR) now dominate reported corporate treasury BTC flows. For macro investors and treasury managers this is more than a headline: it changes how liquidity forms around large trades, how price is discovered during squeezes, and how one should model institutional demand going forward.

This article walks through the evidence, explains the market mechanics altered by concentrated corporate buying, and assesses implications for future ETF competition (including Morgan Stanley’s likely product) and for corporate treasury playbooks.

What the data says: concentration of corporate treasury BTC buying

Multiple market reports point to a clear shift: corporate treasury buying used to be a more dispersed phenomenon — many firms hedging, experimenting, or putting a slice of treasury into BTC. But the latest datasets indicate that MicroStrategy’s purchases now represent an outsized share of that universe.

CryptoQuant-derived reporting compiled by market outlets highlights that Saylor-driven inflows now dwarf other corporate buyers. CoinDesk’s recent coverage makes a similar point, noting that Michael Saylor’s strategy has come to dominate on-chain buying patterns as other firms’ participation collapsed. These pieces together suggest a twin reality: the visible corporate bucket of demand still exists, but it’s been captured largely by a single, repeat buyer. See reporting from CryptoQuant via The Currency Analytics and CoinDesk for the underlying narrative and on-chain snapshots.

How concentration changes liquidity and price discovery

Concentration among corporate buyers affects markets in three practical ways:

Predictability and episodic liquidity: When a single, well-known buyer repeatedly purchases, counterparties can anticipate demand windows and price accordingly. That can compress spreads during known accumulation periods but also concentrate risk outside those windows. A market that expects periodic large buys will trade differently around those events.

Fragile depth and skewed books: Liquidity measured by order book depth can look healthy until you stress it. If many market participants coalesce on the same directional thesis because of a visible corporate buyer, depth can evaporate when the buyer stops or reverses, producing outsized moves on relatively modest flows.

Price discovery distortions: Price discovery relies on diverse, distributed information and capital. A dominant corporate buyer can temporarily decouple price action from broader macro signals. For example, if MSTR adds aggressively during macro weakness, price may stabilize or rally even though macro demand is weak — masking true price discovery and creating a divergence that unwinds later.

These mechanisms are not theoretical. Markets that appear orderly when a dominant buyer is active often become unstable when that buyer pauses. Given MicroStrategy’s size and visibility, the market now reacts not only to BTC fundamentals but to signals about Saylor’s behavior.

Risk vectors for macro investors and treasuries

For macro funds and corporate treasuries evaluating BTC exposure, concentration introduces specific risks to model and mitigate:

Execution risk: Sizing assumptions that rely on continuous institutional demand may be optimistic if a large portion of that demand is from one actor. Treasury managers should stress-test execution slippage under scenarios where concentrated buyers pull back.

Liquidity risk in crisis scenarios: During rapid drawdowns, concentrated holders who cannot or will not sell into thin markets can cause pronounced volatility. Conversely, if they sell quickly, their outsized flows can cascade price moves.

Signaling and governance risk: High-profile corporate buyers change the narrative around corporate crypto allocation. That visibility can attract activist scrutiny, regulatory attention, or peer pressure — all relevant for treasury governance.

Counterparty and custody considerations: A strategy that mirrors or competes with a dominant corporate buyer demands careful counterparty selection and custody strategy to avoid correlated concentration across corporate treasuries.

ETF competition and the Morgan Stanley variable

Concentrated corporate buying is one side of institutional demand; regulated ETFs are another. Morgan Stanley’s imminent Bitcoin ETF has been widely analyzed as a structural demand source that could broaden and institutionalize flows. Recent analysis argues that bank-led ETFs can revive or materially enlarge BTC demand by providing large, low-friction on‑ramp capacity for wealth managers and pensions.

How might a Morgan Stanley ETF interact with Saylor-driven demand?

Demand diversification: ETFs pool diverse end clients, diluting the influence of any one actor. An active ETF rollout could reduce the relative share of corporate-treasury-driven flows and make overall demand less concentrated.

Liquidity provisioning: ETFs tend to institutionalize flows across market makers and authorized participants, which can increase quoted liquidity and improve price formation around large trades. That said, ETFs also concentrate redemption and creation mechanics that can create intraday pressures during stress.

Competitive timing: If an ETF scales quickly, it could crowd out opportunistic counterparties that previously specialized in matching large corporate buys. Conversely, a continuing large corporate buyer like MSTR would still influence directional bias and episodic volatility even as ETFs soak up passive demand.

AmbCrypto’s recent assessment of Morgan Stanley’s prospective ETF launch outlines how a major bank’s product can reshape institutional demand — but it also cautions that ETF demand won’t be a one-to-one substitute for concentrated corporate purchases. The two can coexist and interact in complex ways.

Scenario thinking: three plausible market regimes

To plan, treasuries and macro desks should consider at least three regimes:

Continued concentration: MSTR continues heavy accumulation; corporate treasury demand remains skewed. Markets stay sensitive to Saylor signals; episodic liquidity windows appear around his buys.

ETF-led redistribution: Morgan Stanley and other ETFs scale, diversifying demand. Market depth improves, spreads tighten, and price discovery becomes more macro-driven rather than narrative-driven.

Shock unwind: An adverse event forces a rapid revaluation, and concentrated holders either panic-sell or hold, producing either a cascade or a liquidity vacuum. In this regime, both ETFs and corporate treasuries feel stress — but differences in redemption mechanics may amplify ETF intraday volatility.

Modeling all three outcomes — with probabilities and P&L impact — is a practical way to move from thesis to action.

Practical recommendations for treasury managers

Based on the changed landscape, treasury teams should update policies across five pillars:

Sizing and concentration limits: Cap exposure not only by percent of assets but by scenario-driven liquidity stress tests that assume concentrated opposing flows.

Execution strategy: Use algorithmic execution, time-weighted average price (TWAP) schedules, and diversified counterparties to reduce slippage when liquidity is thin. Consider block trades as well as staggered buys.

Custody and diversification: Prefer multi-custodian strategies and segregated custody to avoid concentration of custody risk that mirrors market concentration.

Disclosure and governance: Update board materials and shareholder communications to explain scenarios around concentrated market participants and to document decision-making frameworks.

Watch ETFs as a liquidity channel: Monitor authorized participant activity and ETF creations/redemptions as an early signal that institutional demand is broadening. Services like Bitlet.app can help teams model installment purchases and compare execution paths.

Conclusion: a new institutional equilibrium

Michael Saylor’s corporate-buying strategy has done more than beef up one company’s balance sheet: it has materially reshaped the institutional demand picture for BTC. Concentration introduces both short-term predictability and long-term fragility. The arrival of institutional ETFs — potentially led by Morgan Stanley — can rebalance that picture, but the interaction will be nuanced.

For macro investors and treasury managers the takeaway is straightforward: don’t treat corporate-treasury demand as a monolithic, stable source. Model for concentration, stress-test liquidity, and build flexible execution and custody frameworks. That is how organizations will navigate a market where public corporate narratives and regulated institutional products compete to set price and liquidity regimes.