WLFI on Dolomite: How Illiquid Collateral and Token Unlocks Created a Margin-Liquidation Time Bomb

Summary

Executive summary

The World Liberty Financial (WLFI) incident on Dolomite is a cautionary case: large stablecoin loans were issued against an illiquid token with high holder concentration and a looming unlock schedule. When price stress began, the combination of poor liquidity, large position sizes, and governance confusion risked turning a borrower default into platform bad debt. This piece breaks down the failure modes, explains why token unlocks and concentration amplified risk, and gives protocol teams and LPs a concrete set of metrics and on‑chain checks to harden lending pools.

What happened (concise recap and why it matters)

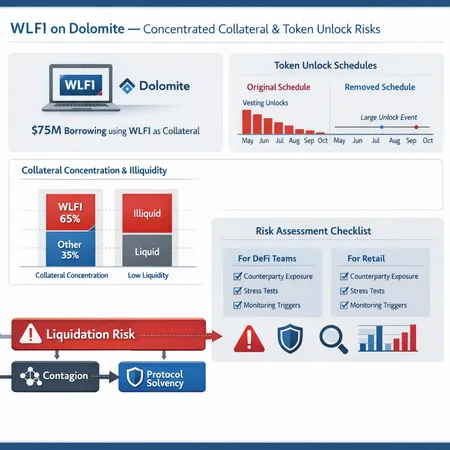

In short: World Liberty Financial borrowed millions of stablecoins on Dolomite using WLFI as collateral. That position relied on WLFI’s market liquidity and the borrower’s ability to defend price, but WLFI is thinly traded and highly concentrated among a few wallets. Reports show the loans and collateral defense prompted market skepticism and a price drop, with the borrow size and collateral composition creating a realistic bad‑debt scenario for Dolomite. See reporting that WLFI dipped after the defended $75 million borrowing and related coverage of the borrowing and unlock controversy for specifics (Cryptopolitan, Bitcoin.com News, Decrypt).

Why this matters for DeFi: when a lending pool accepts concentrated, illiquid collateral at standard LTVs, a few large moves can produce a liquidation cascade — or leave the pool with undercollateralized loans when markets cannot absorb sales without catastrophic slippage.

The compounding factors

- Illiquidity: WLFI’s on‑chain and DEX liquidity were insufficient to support an orderly liquidation of a multi‑million dollar position. Thin order books mean huge slippage.

- Concentration: A small number of wallets controlled a large share of WLFI, magnifying the risk that coordinated selling or a single distressed seller could overwhelm markets.

- Debt scale vs. market depth: The borrowed stablecoins represented a non‑trivial share of tradable value against WLFI.

- Token unlocks and governance noise: Unlock schedules (and even proposals that get proposed then reversed) create uncertainty about future supply; the Decrypt story on an erased unlock proposal underlines how unlocks multiply downside risk by threatening sudden supply additions.

These elements together turn what looks like a collateralized position on paper into a brittle, systemic risk in practice.

Failure modes: how the system can break

Understanding technical failure modes helps design countermeasures.

1) Margin liquidation spiral

If price moves down, automated liquidations try to close positions. In thin markets that forces steep sell orders that further depress price, triggering more liquidations — a feedback loop. The result: the pool recovers far less than expected and lenders face bad debt.

2) Oracle and TWAP latency exploitation

If oracles use stale or manipulable feeds, an attacker (or a panic seller) can create conditions where liquidations execute against prices disconnected from real market depth.

3) Cross‑protocol contagion and defended positions

Borrowers often redeploy borrowed capital elsewhere (leverage, market making, defending price). That creates tangled exposures; if the borrower’s defense fails, both the borrower and any protocol that relied on their intervention are exposed. News coverage documented defensive borrowings around WLFI that increased scrutiny and contagion risk.

4) Unlock cliff supply shock

Large scheduled or potential token unlocks (vests, airdrops, founder releases) introduce the credible threat of sudden supply increases. Even a rumored unlock can induce preemptive selling; an actually executed unlock may be impossible to absorb without crushing price.

What lenders, LPs and DeFi protocols should change

You can apply lessons from WLFI without banning new tokens outright. The aim is to quantify and limit the unique dangers of concentrated, illiquid collateral.

Policy & governance changes

- Enforce debt ceilings per token: hard caps on aggregate borrow exposure for any single collateral token (e.g., 1–3% of total pool value for very illiquid tokens).

- Require vesting‑aware approvals: tokens with unlock schedules should get special scrutiny and lower initial collateral factors.

- Concentration limits: disallow a single holder or linked wallets from supporting >X% of collateralized supply without additional risk mitigants.

Collateral treatment changes

- Liquidity‑adjusted collateral factor (LACF): compute LTVs using a function of market depth, not only price volatility or listed volume.

- Time‑to‑exit haircuts: increase haircuts proportional to the estimated time and slippage required to liquidate a position (see metrics below).

- Dynamic debt ceilings that scale with measured on‑chain liquidity and depth.

Operational & market defenses

- Multi‑oracle TWAPs with minimum update frequency and liquidity weighting.

- Circuit breakers that pause new loans or lower LTVs when a collateral token trips risk thresholds (concentration, unlock cliff, or slippage > threshold).

- Design liquidation auctions that account for thin markets (longer auctions, staged sell‑offs, incentivized buyer pools) instead of immediate market sales.

Recommended metrics and on‑chain checks (actionable)

Risk teams need concrete signals. Here are prioritized checks, suggested formulae, and alert thresholds you can implement as part of lending‑pool risk modules.

- Market depth and slippage profile

- Measure: DEX depth across top pairs (e.g., WLFI/USDC) — the dollar value obtainable with <=5% slippage.

- Rule: require depth >= 5× potential liquidation size for a ‘standard’ collateral factor; if depth < 2×, reduce LTV by 50% or drop token from collateral list.

- Free float vs locked supply and unlock cliffs

- Measure: percent of circulating supply that vests or unlocks within 30/90/180 days.

- Rule: flag if unlock within 90 days >10% of current circulating supply; >25% is a high‑risk emergency requiring immediate LTV reduction.

- Holder concentration index

- Measure: top‑10 holder share; Gini coefficient of holder distribution.

- Rule: top‑10 >30% → reduce collateral factor; top‑3 >50% → typically disallow large borrowings unless mitigants exist.

- Borrower concentration and cross‑exposure

- Measure: share of collateral supplied by single borrower or cluster; cross‑protocol borrowing patterns for the same wallet.

- Rule: cap single‑wallet collateral at e.g., 2% of pool value; flag if the same wallet is simultaneously borrower and liquidity provider elsewhere.

- Borrowed value vs market cap and tradable float

- Measure: outstanding stablecoin borrow / tradable float of the token.

- Rule: if borrow > 5% of tradable float, treat as high risk and lower LTVs or impose debt ceiling.

- Oracle health and staleness

- Measure: time since last oracle update and divergence between on‑chain DEX mid‑price and oracle price.

- Rule: pause liquidations if oracle divergence >5% and not updated for >10 minutes.

- Liquidity inflow/outflow anomalies

- Measure: large incoming transfers to centralized exchanges or bridges; abnormal sell pressure on DEXs (trade size distribution).

- Rule: if detected flows would consume >25% of weekly depth, preemptively tighten borrowing.

- Short‑term supply shock indicator (composite)

- Combine unlock cliff, on‑chain transfers to exchanges, and recent whale sells into a composite score.

- Rule: composite > threshold triggers automatic governance notification and temporary LTV compression.

Operational playbook for rapid response

When a token trips risk thresholds, speed and clarity matter.

- Immediate technical measures

- Pause new borrowings for the token.

- Reduce LTVs for new and, optionally, existing positions gradually (give short notice windows where possible).

- Increase liquidation incentives to attract keepers/bidders.

- Governance and communication

- Activate emergency governance fast track if user funds are at risk.

- Transparently notify LPs and borrowers about the triggers and temporary measures — opacity worsens runs.

- Recovery and remediation

- Use insurance or reserve funds to cover realized shortfalls; coordinate with lenders and insured LPs on apportionment.

- For longer solves, consider debt restructures or negotiated settlements with the borrower only as last resort and with clear governance oversight.

Implementation tips and tooling

- Automate metric collection: integrate on‑chain indexers and DEX aggregators to compute depth and slippage in near real time.

- Dashboards: surface the top signals (depth ratio, unlock cliff %, top‑10 holders) on a single risk dashboard and tie thresholds to governance actions. Tools such as analytics exports or dashboards used by teams like Bitlet.app can be adapted to show these signals alongside positions.

- Backtest thresholds: run historical stress tests using prior episodes (e.g., thinly traded token liquidations) to calibrate multipliers and time windows.

Final takeaways

The WLFI on Dolomite case is not primarily about one token’s politics or narrative — it’s about structural risk: allowing large borrowings against illiquid, concentrated collateral with looming unlocks invites catastrophic slippage and bad debt. Smart risk engineering treats token economics (supply schedules, vesting, holder concentration) and liquidity depth as first‑class inputs to collateral policy.

For DeFi risk teams and LPs: require vesting‑aware collateral factors, enforce strict concentration and depth checks, instrument oracle health, and prepare an operational playbook. These are not optional niceties — they are the difference between a controlled haircut and a platform‑level insolvency event.

Sources

- World Liberty Financial borrowing coverage and collateral defense: World Liberty Financial borrows millions on Dolomite, defends WLFI collateral

- Market reaction and token dip reporting: WLFI token dips 10% after defended $75M stablecoin borrow

- Unlock proposal controversy and bad‑debt concerns: Trump‑linked WLFI erases $427 million token unlock proposal amid DeFi loan concerns