WLFI on Dolomite: How Concentrated Collateral and Token Unlocks Threaten DeFi Protocol Solvency

Summary

Executive overview

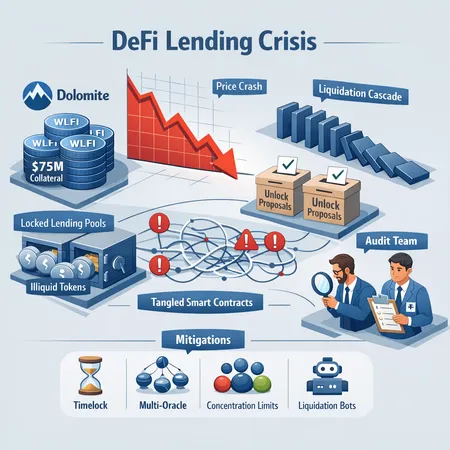

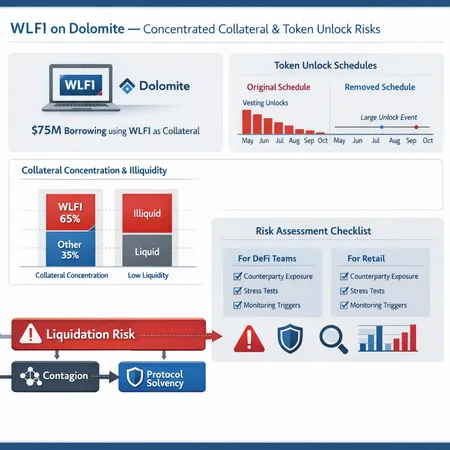

The recent World Liberty Financial (WLFI) activity on Dolomite — a defended $75 million borrowing secured with WLFI and the subsequent controversy around a proposed $427 million token unlock that was later erased — is a textbook case of concentrated-collateral risk in DeFi lending. Beyond headlines, the episode illuminates how illiquid collateral, opaque counterparty behavior, and changing unlock schedules can combine to create acute liquidation and protocol solvency pressure.

This article dissects the mechanics behind the event, explains why concentrated collateral matters, and delivers an actionable framework risk teams and retail users can use to evaluate counterparty exposure. For context on the original events, see coverage by Cryptopolitan, Bitcoin.com, and Decrypt.

What happened: WLFI borrowing and the unlock saga (brief timeline)

- World Liberty Financial took large loans on Dolomite using WLFI tokens as collateral; public reporting notes a defended borrowing of roughly $75M against WLFI collateral. See the initial coverage at Cryptopolitan for the $75M detail and Bitcoin.com for collateral specifics.

- Later, a separate governance proposal for a sizable WLFI token unlock (reported at $427M) was introduced and then erased amid community backlash and systemic concern. Decrypt provides a follow-up explaining the erased unlock proposal and the broader implications.

Together these events exposed two linked issues: (1) heavy borrowing secured by a concentrated, relatively illiquid token; and (2) sudden changes to token unlock schedules that shift the market incentives for selling or holding.

Why concentrated, illiquid collateral is dangerous for lending protocols

When a lending position represents a large fraction of a token’s liquid supply or when that token has limited market depth, normal assumptions behind collateral valuation break down. Here’s why that matters:

1) Price impact and liquidation spirals

If a borrower is forced to sell collateral, large sell orders on a thin market can move price dramatically. That price decline can trigger on-chain liquidations, which push prices down further — a classic liquidation spiral. In extreme cases, the protocol’s safety buffer isn’t enough and insolvency follows.

2) Difficulty of close-out and recovery

Protocols assume the ability to auction or sell collateral into the market at roughly spot. With concentrated collateral, recoverable value is a function of market depth, not just quoted price. If a single counterparty holds or controls a large portion of tokens pledged as collateral, unwind options are limited.

3) Correlated counterparty risk

Large, concentrated borrowers are often connected to other positions and protocols. If one big holder is stressed, contagion can propagate across lending platforms, market makers, and DEX pools.

4) Governance and moral hazard

When token supply and governance are concentrated, insiders can influence both tokenomics (like unlock schedules) and lending behavior. That can create moral hazard where insiders take outsized risk, knowing they can later alter token rules.

Token unlock schedules: why they matter and what removing an unlock does

Token unlocks define when vested tokens enter the free float. That schedule is a forward-looking supply shock; markets price expected unlocks well in advance. Two mechanisms matter:

- Sell pressure: unlocks increase available supply and often translate into selling, especially if unlock beneficiaries seek liquidity.

- Price expectations: the mere possibility of a large unlock can suppress bids and reduce liquidity depth even before tokens hit market.

Removing or erasing an unlock proposal — as happened around WLFI — changes short-term incentives. It may reduce near-term sell pressure, potentially improving price and collateral valuations. But it also creates longer-term uncertainty: are there undisclosed backstops, or will unlocks be reintroduced later? That ambiguity can obscure true counterparty exposure and leave protocols complacent.

The Decrypt follow-up on the erased $427M proposal highlights this point: removing an unlock sounds stabilizing, but it masks underlying supply concentration and governance centralization.

Measuring the risk: practical metrics and signs for DeFi risk teams

Below are concrete, monitorable metrics that should be part of any lending-risk dashboard when assessing borrowers and collateral tokens like WLFI.

A. Collateral concentration metrics

- Percentage of circulating supply used as collateral: percentCollateral = collateralLocked / circulatingSupply. Values above 2–5% require heightened scrutiny; above ~10% are usually dangerous for illiquid tokens.

- Top-10 holder share: if top 10 addresses control >30–50% of supply, expect governance and market-manipulation risk.

- Largest single collateral position share: a single borrower holding >3–5% of float in pledged collateral is a red flag.

B. Liquidity and market depth

- Order-book depth across primary DEXs/DEX aggregators: measure expected price impact for sell sizes equal to collateral value (e.g., what slippage to sell $10M worth?).

- 24h traded volume vs. collateral value ratio: low ratios (volume << collateral size) mean you cannot liquidate safely.

- Concentration by venue: if most liquidity sits in a single AMM pair with low TVL, liquidation options are thin.

C. Unlock and vesting transparency

- On-chain vesting contracts: verify schedules and beneficiaries on-chain. A disappeared or altered unlock request should trigger an audit and on-chain proofs.

- Unlock cliffs vs. linear vesting: cliffs are more dangerous. A single large cliff can overwhelm markets.

D. Counterparty behavioral signals

- Sudden increases in borrow size or collateral posting frequency.

- Changes in collateral composition (moving to more illiquid tokens without commensurate risk premiums).

- Governance actions altering token supply or vesting rules.

E. Protocol-level exposure

- Total exposure to token X across the protocol (loans outstanding, collateral posted, insurance fund size). Compare to protocol reserves.

- Simulated stress tests: run liquidation scenarios with price impact models rather than assuming spot prices.

Tools and modeling approaches (practical)

- Slippage curves: generate expected slippage vs. trade size using AMM constant-product math or aggregated order book models. Integrate these into liquidation engines.

- Scenario-based stress tests: model 10%, 30%, and 60% price shocks combined with varying sell-side liquidity to estimate shortfalls.

- Counterparty scorecards: combine on-chain metrics (top-holder share, collateral % of float) with behavioral flags to derive a composite risk score.

- Watchlists and alerting: set thresholds for sudden collateral concentration growth and governance changes (e.g., new unlock proposals).

Open-source tooling (Etherscan, Dune queries, Dex data aggregators) plus some custom TVL/depth scrapers are often sufficient to build these dashboards.

For retail users: a practical checklist before accepting loans or lending on a pool

- Check collateral composition: Is the collateral token widely traded with consistent depth? If a single token dominates collateral, ask why.

- Verify vesting contracts: who benefits, and when do tokens unlock? Look at on-chain vesting, not just forum posts.

- Evaluate liquidation path: ask or test how the protocol plans to liquidate collateral (auctions, on-chain swaps). Would liquidation materially move price?

- Size your exposure: don't accept a loan that would require selling more than a few percent of a token's daily volume to close.

- Diversify collateral and counterparties: reduce tail risk from any one concentrated borrower.

Retail users can use the same public metrics risk teams do — circulating supply vs. collateral, top-holder concentration, and trade-depth checks are all tractable on-chain.

Governance and transparency best practices for protocols

Protocols managing lending markets should adopt minimum standards:

- Collateral limits per token: hard caps on collateral exposure relative to circulating supply and protocol TVL.

- Dynamic collateral factors: reduce collateral factor for tokens with poor depth or high concentration.

- On-chain vesting verification: require cryptographic proof of vesting schedules before accepting a token as collateral.

- Emergency circuit breakers: automatic suspension of new borrowing against a token if its collateral share grows past a threshold.

- Public counterparty dashboards: show large borrower positions, collateral composition, and protocol exposure in real time.

These measures force protocols to price concentration risk explicitly instead of hoping diversification or goodwill will save them.

Applying the framework to WLFI on Dolomite (illustrative)

Based on reporting, WLFI borrowing on Dolomite reached a scale (€75M reported) that — had WLFI been illiquid relative to that loan size — would put the protocol at notable risk. Key checks that should have been performed:

- Calculate WLFI collateral share of circulating supply and compare to recommended thresholds.

- Model liquidation slippage for selling $75M of WLFI across the major pools and DEXes.

- Confirm transparency of any token unlocks and governance changes; the erased $427M proposal should have triggered an immediate forensic review and stress re-run.

The combination of a large borrow and a contested unlock proposal is precisely the mix that turns a single counterparty incident into a systemic solvency stress.

Quick decision rules for risk teams (one-page summary)

- If percentCollateral > 5% of circulating supply: cap new borrowing and require overcollateralization >150%.

- If largest holder > 30% AND top-3 holders control >50%: downgrade collateral factor and require an independent market maker commitment.

- If expected liquidation trade size causes >15% realized slippage: add liquidation penalty buffer or refuse token as primary collateral.

- If unlock proposals larger than 10% of circulating supply are pending: treat as equivalent to a near-term supply shock in stress tests.

Final thoughts and context

Concentrated collateral and token unlock dynamics are not theoretical — the WLFI episode on Dolomite demonstrates how governance, disclosure, and market structure interact to create solvency risk. Removing an unlock proposal can calm markets briefly, but it doesn't eliminate underlying concentration. That’s the core lesson for both DeFi risk teams and retail users.

Protocols should bake in concentration-aware rules and transparent monitoring, and users should demand visibility before trusting an asset as collateral. Tools and watchlists exist to make this practical; the only missing ingredient in too many markets is discipline.

For more on lending risk and building monitoring dashboards, practitioners can also look at related work on platform risk and market microstructure. Bitlet.app publishes tooling and educational resources that can help teams implement some of these checks in deployment.

Sources

- Initial report of WLFI token dipping after defense of a $75M stablecoin borrowing deal on Dolomite: Cryptopolitan

- Detailed account of World Liberty Financial’s multi‑million borrowing and collateral specifics: Bitcoin.com

- Follow-up on the erased $427M token unlock proposal and systemic concerns for Dolomite: Decrypt

For broader context on how markets react to concentrated supply and governance actions, consider monitoring on-chain analytics and community governance forums. And remember: when a token’s floating supply and collateral use are tightly linked, protocol solvency becomes a market‑structure problem — not just a price one.

For readers keeping tabs on cross-market signals, insights from DeFi analytics and macro narratives in Bitcoin can be useful complements to this framework.