Tether, USDT Supply and the Evolving Health of the Stablecoin Market

Summary

Executive snapshot: profit, supply, and what’s changed

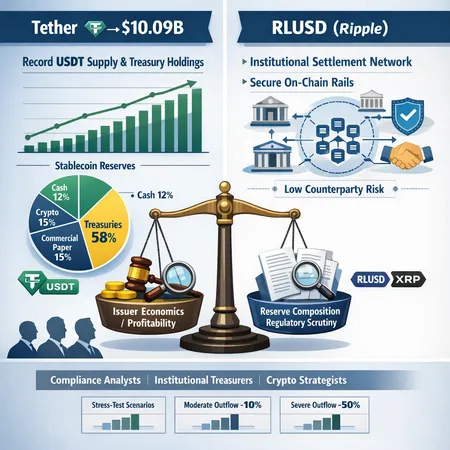

Tether’s 2025 disclosures show a familiar paradox: USDT supply hitting a new record while issuer profitability softens. Tether reported net profit of about $10.09 billion, down roughly 23% year‑over‑year, even as circulating USDT expanded to an estimated $186 billion and the firm’s treasury holdings climbed to $122 billion. These are not trivial statistics — they alter issuer economics, reshape counterparty signals and amplify regulatory attention.

For macro context: many traders still view Bitcoin as the primary market bellwether, but stablecoins like USDT increasingly operate as the plumbing of crypto markets. That plumbing now carries higher absolute exposure and slightly thinner margins.

How to read the 2025 numbers: profitability vs scale

Tether’s profit decline (reported by several outlets) coincides with record scale. Two observations matter:

- Scale doesn’t guarantee margin expansion. Larger USDT supply increases absolute interest‑bearing assets required to backredemptions, but yields on safe instruments have been volatile and, in many jurisdictions, compressed by market competition and central bank moves.

- Treasury holdings rose as a liquidity buffer. Tether reported record treasury holdings (~$122B), a deliberate tilt toward high‑quality, liquid assets to reassure markets and regulators.

Taken together, the picture is consistent with a business that is larger, more liquid, but operating with lower risk‑adjusted profitability. Coverage of the financials can be found at Cryptopolitan and CryptoNews, while the USDT supply milestone was reported by Coinpedia.

What the profit drop means for issuer economics

A 23% decline in net profit implies pressure on one or several of the issuer’s revenue levers:

- Lower yield on reserves. If a greater share of reserves is parked in ultra‑liquid, low‑yield instruments (short‑dated treasuries, cash), interest income falls.

- Higher operating or compliance costs. Post‑crypto collapse regulatory frameworks and KYC/AML programs increase fixed costs for firms operating at scale.

- Spread compression. Competition from other stablecoins and institutional products (including bank‑backed rails) compresses the effective margin between assets backing stablecoins and redemption liabilities.

For compliance teams and institutional treasurers this matters: declining profitability can subtly shift incentive structures — e.g., preferences for higher‑yield (but less liquid) reserve allocations to sustain margins, or a push to monetize treasury holdings in ways that increase market exposure.

Reserve composition, treasury holdings and regulatory scrutiny

Tether’s reported growth in treasury holdings is a double‑edged sword. On one hand, shifting reserves toward cash and government securities increases near‑term liquidity and reduces reliance on opaque credit instruments. On the other, concentrating $122B in tradable securities ties issuer solvency to market liquidity and repo or interest‑rate shocks.

Regulators care about three dimensions:

- Liquidity coverage: Can the issuer meet large, rapid redemptions without fire‑selling assets? High treasury holdings improve coverage but only if those assets can be monetized quickly.

- Transparency and auditability: Market confidence responds to verifiable proofs of reserves and third‑party attestations; uncertainty invites regulatory intervention.

- Concentration risk: Large holdings in particular instruments or counterparties create systemic spillovers.

If regulators push for higher transparency or restrict certain asset classes from reserve eligibility, issuers may need to reallocate into shorter‑duration instruments — improving safety but reducing yield, which feeds back into profitability.

New entrant designs: how RLUSD differs from USDT

While USDT follows a generalized issuer‑backed model, Ripple’s RLUSD is positioned differently, targeting institutional settlement and collateral use cases. Key contrasts:

- Target audience: USDT aims across retail, exchange and institutional flows; RLUSD is explicitly marketed for payments/settlement and institutional collateral (per analysis at Bitcoinist).

- Design tradeoffs: RLUSD proposals emphasize integration with settlement rails and counterparty protections for financial institutions, which can reduce systemic fungibility compared with ubiquitous tokens like USDT.

- Counterparty model: RLUSD’s tie to Ripple and potential settlement partnerships may offer different legal recourse and operational integrations than Tether’s model.

From a treasurer’s perspective, RLUSD may be attractive where institutional settlement guarantees, legal clarity and tighter counterparty agreements matter more than broad liquidity on secondary markets.

Implications for traders, treasurers and compliance teams

Traders: USDT’s deep liquidity will likely persist, but watch for basis volatility during stress episodes if reserve holdings must be monetized. Diversifying access across stablecoins (and keeping on‑chain and off‑chain rails) reduces single‑counterparty exposure.

Institutional treasurers: The rise in USDT supply increases available stable liquidity, but counterparty risk is non‑negligible. For treasury uses (collateral, settlement), evaluate alternatives like RLUSD and bank‑native settlement tokens, especially where legal contract certainty and sessioned settlement matter.

Compliance teams: Expect regulators to press for clearer reserve composition disclosures and perhaps limits on what counts as an eligible reserve. Prepare to adapt AML/KYC and counterparty exposure limits; build scenarios that link reserve asset liquidity to redemption stress.

Bitlet.app users and institutional clients should factor stablecoin counterparty risk into treasury dashboards and daily liquidity stress tests.

Data‑driven reserve stress‑testing: three scenarios

Below are illustrative stress tests using the public datapoints: USDT supply ~$186B and treasury holdings ~$122B. These are simplified models to demonstrate sensitivities — treat them as frameworks to adapt with internal balance‑sheet data.

Assumptions for all scenarios:

- Total USDT outstanding (liabilities): 186,000,000,000

- Treasury holdings: 122,000,000,000 (liquid assets that can be monetized within 1–3 days)

- Other reserves (credit instruments, commercial paper, cash equivalents): 64,000,000,000

- Redemption rate shock: percentage of supply redeemed in 7 days

Scenario A — Mild run (20% redemption in 7 days)

- Redemption demand: 0.20 × 186B = 37.2B

- Treasury can cover: 122B > 37.2B — result: Covered without tapping less‑liquid reserves. Market impact: low.

Scenario B — Severe run (40% redemption in 7 days)

- Redemption demand: 74.4B

- Treasury can cover: 122B > 74.4B — still covered on paper, but monetizing $74.4B of treasuries over short windows may widen bid/ask spreads and push yields up; if a portion (say 30%) of treasury holdings are encumbered or subject to settlement lag, realized coverage drops and issuer may need to liquidate commercial paper or other assets at a discount.

Scenario C — Extreme run with market‑liquidity shock (50% redemption and 25% of treasury temporarily illiquid)

- Redemption demand: 93B

- Available treasury (adjusted for illiquidity): 0.75 × 122B = 91.5B

- Shortfall: 1.5B — issuer must use other reserves or emergency lines. If other reserves are credit‑sensitive and price‑dislocated, losses and haircuts may be realized; profit margins and capital buffers will be stressed.

Key takeaways from scenarios:

- Large treasury holdings materially raise nominal coverage, but operational encumbrances and market liquidity determine real coverage.

- Profitability declines (lower earnings) reduce the issuer’s buffer to absorb trading losses or liquidity windows.

- Compliance-led limits (e.g., concentration caps) can reduce available immediate liquidity, improving safety but increasing cost.

Monitoring checklist and early warning indicators

To operationalize risk monitoring, compliance teams and treasurers should build a dashboard with the following metrics:

- Daily USDT supply and net flows; track top counterparties and exchange‑level concentration.

- Composition of reserves by liquidity bucket (0–3 days, 4–30 days, >30 days) and encumbrance status.

- Market depth for primary treasury instruments (bid/ask spreads, recent auction sizes) and repo market access indicators.

- Profitability drivers for the issuer (quarterly net profit trends, yield on treasury holdings) — declining profitability may precede riskier asset allocations.

- Regulatory filings and attestation frequency; any pause or reduction in attestations is a red flag.

Strategic recommendations

- For traders: keep trading lines across multiple stablecoins and maintain margin buffers to avoid forced liquidation during basis shocks.

- For treasurers: prioritize counterparty diversity and legal certainty when using stablecoins as collateral; pilot institutional settlement tokens like RLUSD for high‑value, contractual flows.

- For compliance teams: insist on granular reserve disclosures from counterparties and test those disclosures via market‑based liquidity simulations.

Conclusion: fragility in scale, resilience in transparency

Tether’s 2025 financials underscore a structural pivot: the stablecoin market is now enormous, but not immune to margin pressure and regulatory dynamics. Record USDT supply and rising treasury holdings improve headline liquidity but also concentrate exposures. Profits falling by roughly 23% reflect compressed margins and higher costs, which can influence reserve choices and risk appetite.

New models like RLUSD aim to capture institutional settlement needs with different counterparty constructs; they won’t instantly replace USDT’s on‑chain ubiquity but offer useful alternatives for high‑assurance use cases. For compliance analysts, institutional treasurers and strategists, the practical lesson is clear: measure liquidity in operational terms, not headline dollars, and build monitoring that captures both market and regulatory shocks.

Sources