How to Stress‑Test Token Unlocks: Modeling Short‑Term Supply Risk for HYPE and RAIN

Summary

Why token unlocks matter now: the mechanics and the magnitude

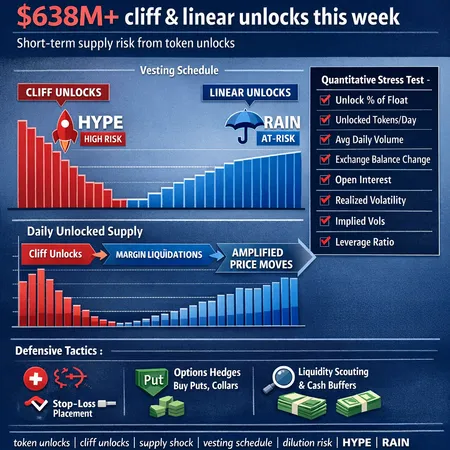

Token unlocks are scheduled releases of previously locked or vested coins into circulation. They come in two common shapes: cliff unlocks (a one‑time release) and linear unlocks (a steady drip over a period). Both increase available supply, but cliffs create sudden supply shocks that can amplify price moves, while linear schedules increase baseline dilution risk over time. Blockonomi’s weekly tracker shows $638M+ set to hit markets across cliff and linear unlocks this week, a reminder that calendar risk is real and concentrated.

Unlocks are a market microstructure event, not just an accounting line. If unlocked tokens flow to exchanges or OTC desks quickly, they compete with existing sellers and can widen spreads, reduce depth, and trigger stop‑losses and margin liquidations. In stressed markets these mechanics interact with macro shocks and derivative leverage to create outsized moves—exactly what traders want to model and guard against.

How unlock schedules interact with liquidations and macro shocks

A scheduled unlock becomes dangerous when it coincides with: weak liquidity, concentrated vested holdings, high open interest in derivatives, or a larger macro event (for example, a Bitcoin correction). That combination creates a loop:

- Price drops slightly → funding and margin pressure rises → forced liquidations occur → sell pressure intensifies → unlocked supply is monetized into an illiquid market → further price weakening.

- Cliff unlocks accelerate the first step by adding a large, immediate buffer of sellers. Linear unlocks lengthen the window of vulnerability and can keep volatility elevated.

Crypto history is full of examples where altcoins plunged more than peers once BTC fell and liquidity dried up; a recent market watch lists several altcoins that suffered deeply during BTC‑led sell‑offs, which illustrates how sensitive smaller tokens can be to cascading liquidity events. See that analysis for concrete cases and to gauge how correlation and leverage amplify moves in practice.

Which tokens are most at risk this week: HYPE and RAIN (what to look for)

HYPE and RAIN are both scheduled in unlock calendars this week and merit extra attention. Risk factors that make a token like HYPE or RAIN vulnerable:

- Small market cap or narrow free float relative to the unlocked amount.

- Low daily traded volume (ADV) so even moderate sell-through causes large price moves.

- High concentration of vested tokens to a small number of wallets (founders/VCs) that may opt to liquidate.

- Presence of leveraged retail or concentrated futures positions (high open interest / mark price sensitivity).

You don’t need exact privileged data to act—combine on‑chain vesting info with order‑book checks and ADV to build a sufficient risk picture. If you’re tracking many positions, flag tokens with (UnlockedAmount / FreeFloat) > 5–10% or (UnlockedAmount / ADV) > 1–3x as elevated risk and escalate them to a stress test.

A quantitative checklist to estimate dilution and price‑impact risk

Below is a repeatable checklist you can run quickly for any unlock event. Use conservative assumptions in stressed scenarios.

Gather the basics

- Total unlocked amount (U)

- Current circulating supply / free float (F)

- Market capitalization (MC) = Price × Circulating supply

- Average daily volume (ADV)

- Best bid/ask depth at X% (order book depth to absorb U)

- Open interest and major futures leverage metrics

Compute raw dilution

- Immediate dilution % (if sold into market) = U / (F + U).

- Example: if F = 100M tokens and U = 10M, dilution = 10/110 = 9.1%.

Compare to liquidity

- Unlock vs ADV = U / ADV. If > 1x, selling the full unlock into a single day will probably move price a lot.

- Order book absorption ratio = U / (sum of passive bids within N% from mid). If > 0.5, expect big slippage.

Estimate price impact (simple market‑impact math)

- Conservative square‑root model: Impact % ≈ k × sqrt(Q / ADV), where Q is quantity sold and k is a market‑specific constant (0.7–1.5 for thin altcoins; use 1.0 as a working conservative baseline).

- Example (hypothetical): Q = 5M tokens, ADV = 1M tokens, k = 1 → Impact ≈ 1 × sqrt(5) ≈ 2.24 → ~224% implied—this tells you selling Q into one day would devastate the market. In practice, price would gap down well beyond simple arithmetic because bids vanish.

Incorporate derivative/leverage feedback

- Estimate percentage of longs that would be liquidated at given price moves by checking funding, open interest, and typical liquidation thresholds.

- Model cascades: a 20% price drop that liquidates 30% of open interest could add another X% of selling pressure, compounding the initial impact.

Stress scenarios

- Base case: 20–50% of U sold over 7 days into normal ADV.

- Stressed case: 50–100% of U sold immediately into 0.5× ADV with a concurrent macro shock (BTC −10%).

- Run both and observe resulting NAV change; use the worse outcome for sizing hedges.

Practical example (hypothetical HYPE case) — run the numbers fast

Assume: F = 100M tokens, Price = $0.50 → MC = $50M. U = 10M tokens (unlocked), ADV = 2M tokens.

- Immediate dilution = 10 / (100 + 10) = 9.1%.

- Unlock vs ADV = 10 / 2 = 5× (highly risky).

- Square‑root impact (k = 1): Impact = sqrt(5) ≈ 2.24 → naive model implies >100% price move to clear that selling into one day, i.e., market would experience a very large gap. Even selling 20% of U into a single day (2M tokens) would be 1× ADV and likely push price tens of percent.

This crude math shows you should not assume linear absorption—order books for small tokens are lumpy and will vanish under stress. Use these scenarios to set hedges and size reductions.

Defensive tactics: stop‑losses, options hedges, and liquidity scouting

Below are practical, executable defenses ranked by cost and speed.

1) Reduce leverage and position size ahead of unlocks

- The cheapest defense is to reduce exposure: lower position size or deleverage entirely if the unlock/dilution risk exceeds your tolerance.

- If you must stay long, scale exposure to worst‑case NAV hit from stress scenarios.

2) Staged exit and OTC liquidity

- Avoid executing the entire reaction on public order books. Use OTC desks for large blocks or staged limit orders to avoid sweeping the book.

- Pre‑arrange block liquidity windows when possible; this is particularly effective for institutional-sized unlocks.

3) Smart stop‑loss placement

- Don’t set stops as a simple percent of price alone. Tie stop levels to liquidity metrics—for example, set stops below levels where cumulative passive bids drop below X% of your position.

- Use ATR or expected microstructure noise: typical guidance is stops at 1.5–3× short‑term ATR in liquid markets. For thin tokens widen that multiple and combine with conditional or TWAP exit plans to avoid cascade selling.

4) Options hedges and collars

- Buy near‑term puts with strikes close to your risk tolerance (e.g., −10% or −20%) to cap downside during the unlock window. If puts are expensive, use collars: sell OTM calls to finance puts.

- For tokens without liquid options, synthetics (short futures + long spot) or tail hedges on correlated liquid proxies may help (e.g., index or base layer hedges). Keep in mind correlation decay.

5) Shorting / derivative hedges

- Take short positions in futures where available, sized to absorb modeled NAV change. Watch funding rates and liquidation structure—shorts can be costly if funding turns against you or if liquidity for closing shorts vanishes.

6) Liquidity scouting and order‑book monitoring

- Real‑time checks: aggregate DEX pool depths, centralized exchange book depths, and small‑order fills to map where liquidity sits.

- Watch for early signs: sudden increases in sell-side limit orders or large wallet moves to exchanges often precede stronger selling.

7) Communication and governance engagement (if applicable)

- For concentrated positions, engage with teams or large holders if possible—sometimes lockups are restructured, or large holders stagger sales following negotiation. This is more relevant to VCs or institutional counterparties.

Putting it together: an execution plan for portfolio managers

- Calendarize: build an unlock calendar and flag tokens with U / F > 5% or U / ADV > 1×.

- Run quick scenario math for base and stressed cases using the checklist above.

- Decide defensives by cost: (a) reduce size, (b) OTC / staged exit, (c) buy puts or collar, (d) short futures / margins, (e) widen stops tied to liquidity.

- Pre‑position if cost‑effective: options often spike before unlocks because others hedge; weigh cost vs protection.

- Monitor in real time: order book depth, on‑chain flows, exchange inflows, and funding/ OI shifts.

- Execute contingency: if price moves beyond scenario thresholds, trigger pre‑planned exits or hedges.

This repeatable framework reduces decision friction during noisy windows. Platforms like Bitlet.app can help with scheduled rebalancing and execution primitives, but the real work is in the pre-event quantification and playbook.

Final checklist (one‑page quick reference)

- Unlock amount U? Free float F? ADV? Order book depth?

- Is the unlock cliff or linear? (cliff = higher short‑term risk)

- U / (F + U) → dilution percentage

- U / ADV → execution risk multiple

- Open interest / derivative leverage exposure

- Holder concentration / on‑chain transfer risk

- Hedging plan: options, shorts, OTC, staged exit

- Execution triggers and fallback plans

Sources

- Blockonomi — weekly tracker of token unlocks and schedule details: Crypto token unlocks this week — $638M set to hit the market

- CryptoPotato — market watch on altcoins that suffered during BTC declines and the mechanics of sell‑offs: These altcoins suffered the most as Bitcoin fell to new local lows