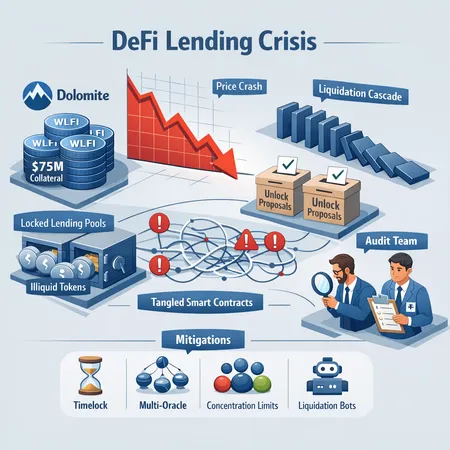

The WLFI/Dolomite Fallout: What Concentrated Collateral Reveals About Counterparty Risk in DeFi

Summary

Quick framing

The WLFI/Dolomite episode is a compact lesson in classic DeFi failure modes: large, concentrated collateral, opaque counterparty exposure, and governance friction when markets move. In late-stage events, World Liberty Financial (WLFI) used WLFI tokens as collateral for a multi‑million dollar stablecoin borrowing on Dolomite; the market reaction and subsequent governance proposals pushed the token price lower and left lending pools facing the risk of illiquid collateral and potential bad debt. For risk teams and auditors, the narrative is useful because it shows how protocol primitives and human governance interact under stress — and why many of the theoretical mitigants are only as good as their implementation. (Bitlet.app users concerned about counterparty exposure have started asking the same questions.)

Timeline: the borrow, the dip, and governance drama

The critical sequence is short but consequential. Reports indicate World Liberty Financial borrowed against WLFI collateral, resulting in roughly a $75 million exposure denominated in stablecoins on Dolomite. Coverage surfaced fast — News.Bitcoin reported on the multi‑million borrow and WLFI’s public defense of the collateralization choice, while Cryptopolitan captured immediate market reaction as WLFI’s price dipped after the announcement. Later, a contentious token unlock proposal — reportedly amounting to hundreds of millions of dollars in potential WLFI unlocks — was discussed and ultimately erased amid concerns it would exacerbate bad debt for lenders, as covered by Decrypt.

Taken together: a large loan backed by a single, thinly traded token; public scrutiny and defensive messaging from the borrower; a measurable price decline; and a governance fight over unlocks that could have produced a massive sell pressure. That chain is enough to push a lending pool from healthy to stressed if it lacks proper limits or fallback mechanisms.

How a $75M borrow against WLFI collateral works — and why it scares lenders

At a basic level, DeFi lending platforms accept tokens as collateral and allow borrowing against a risk-weighted value of that collateral. The problems in this case were structural:

- Single‑token collateral: WLFI was used as a primary backing asset. When one token represents a large share of loans outstanding, the pool’s solvency becomes correlated with that token’s market liquidity and price stability.

- Valuation and oracles: The borrowed amount depends on on‑chain prices. If oracles are slow, manipulable, or rely on thinly traded markets, the system can overvalue collateral shortly before a crash.

- Concentration of counterparty exposure: If a single borrower or affiliated entity holds the majority of debt, the protocol inherits idiosyncratic counterparty risk (not just market risk).

Dolomite’s case highlights all three vectors. When the borrower’s defense and external rumors catalyzed selling pressure, WLFI’s market price dipped. That drop directly reduced the effective collateral value and increased liquidation pressure — except when the collateral itself is illiquid enough that liquidators cannot exit positions without collapsing the price further.

Why single‑token collateral concentration is especially dangerous

Concentrated collateral magnifies two interconnected threats:

- Market impact on liquidation: If large loan health depends on a token with shallow order books, attempts to liquidate will move the market dramatically. A cascading waterfall of forced sell orders can render liquidation suboptimal or impossible.

- Governance and social friction: Big holders can influence protocol governance, delays in emergency votes can freeze risk remediation, and token unlock events (or proposed unlocks) can create sudden supply shocks.

The Decrypt report explains how an erased $427 million unlock proposal created fresh concerns about bad debt on the lending protocol — a classic example of governance proposals themselves becoming a risk vector. When a large unlock is on the table, token holders may rush to sell or otherwise reposition, amplifying liquidation risk even before any on‑chain liquidations begin.

How lending pools get stuck with illiquid collateral (the mechanics)

There are a few common paths from a stressed loan to real bad debt:

- Underwater loans with illiquid collateral: The collateral’s mark price (oracle) drops below the liquidation threshold, but market depth is insufficient for liquidators to buy and sell without extreme slippage. Liquidators either fail to monetize collateral or choose to stop bidding, leaving the pool with assets it cannot convert to the borrowed currency.

- Oracle lag and manipulation: Oracles that report stale or manipulable prices can temporarily mask distress, creating sudden reverts when an oracle update reflects reality. Conversely, oracles that are too responsive to thin liquidity can be spoofed to trigger liquidations.

- Governance lag: Emergency response — whether to adjust collateral factors, trigger auctions, or whitelist alternative liquidators — requires governance action. If governance is slow or contentious, the window to prevent cascading defaults may close.

When these factors combine, the protocol faces two bad options: accept the illiquid tokens on its balance sheet (taking a haircut later) or trigger fire‑sale liquidations that destroy market value and reputation.

Mitigations: governance and technical safeguards (what protocols should adopt)

Below are practical mitigations, split into design and governance elements. Each is widely discussed in risk literature but worth re-emphasizing in light of WLFI/Dolomite.

Oracle design and multi-source pricing

Use multi‑source oracles with liquidity‑weighted aggregation and TWAP (time‑weighted average price) fallbacks to minimize flash‑manipulation risk. Implement circuit breakers for price feeds when the deviation between sources exceeds a tolerance band.

Collateral baskets and concentration caps

Limit the percentage of a borrow book that can be collateralized by a single token and require diversified collateral baskets for large loans. Enforce hard caps on exposure to any single issuer or holder group to prevent idiosyncratic counterparty failure from threatening the whole pool.

Dynamic collateral factors and haircut policy

Tie collateral factors and maximum LTVs to on‑chain liquidity metrics (e.g., 24‑hour depth, realized slippage). Reduce allowable LTV for tokens with low liquidity or high holder concentration. Make haircuts automatic based on transparent, auditable metrics.

Automated liquidation algorithms and decentralized liquidators

Design liquidations that account for market depth. Implement partial or incremental liquidation strategies rather than single‑shot auctions. Encourage a diverse set of market‑making liquidators and consider incentivizing them with fee rebates or subsidized gas to participate in stressed conditions.

Emergency modules, debt auctions, and bonding curves

Have pre‑audited emergency modules that can trigger auctions, debt auctions, or temporary circuit breakers. Auctions should be parameterized and tested in stress scenarios; they must be able to handle illiquid collateral by allowing extended bidding windows, multi‑asset bids, or structured settlement periods.

Governance limits and time‑locked actions

Prevent immediate large‑scale unlocks or parameter changes that can supply sudden sell pressure. Use multi‑stakeholder timelocks for high‑impact proposals and require quorum and supermajority thresholds for actions that materially affect collateral supply or valuation.

On‑chain transparency and counterparty disclosure

Require large borrowers or governance actors to disclose related‑party positions and collateral provenance. Protocols should enforce KYC/AML standards where appropriate for centralized counterparties and at least maintain clear on‑chain provenance checks for large collateral deposits.

Regular audits and scenario stress tests

Auditors must model concentrated collateral stress tests and liquidity shocks in their reports. An audit that only checks code correctness but not realistic economic attack vectors is incomplete. Insist on continuous monitoring dashboards showing concentration metrics and stress test outcomes.

Practical checklist for DeFi lenders, auditors, and risk teams

- Enforce maximum exposure limits to any single token and to any single counterparty.

- Require diversified collateral for large loans and discount concentrated positions more aggressively.

- Test oracles under low‑liquidity conditions; simulate manipulation vectors in audits.

- Design incremental liquidation logic and pre‑authorize emergency auction parameters.

- Build governance friction for high‑impact token unlocks (timelocks, higher thresholds).

- Maintain an on‑chain and off‑chain alerting stack for concentration metrics (e.g., % of circulating supply used as collateral).

- Include scenario‑based capital buffers or insurance funds sized by stress‑tested bad‑debt estimates.

What WLFI/Dolomite reveals about systemic DeFi risk

The incident is a reminder that DeFi combines smart contracts with real markets and human governance. Code correctness alone does not immunize a protocol from market illiquidity or governance‑driven supply shocks. The erased unlock proposal covered by Decrypt and the price reaction covered by Cryptopolitan illustrate how governance proposals and public signaling can be as dangerous as on‑chain exploits. Auditors and risk teams must therefore treat governance events, concentration metrics, and oracle architecture as first‑class audit items.

For many participants, the WLFI story reads like a checklist of avoidable mistakes: large single‑token exposure, inadequate oracle/circuit breaker design, insufficient governance friction on unlocks, and weak contingency tooling for auctions or emergency liquidations. The remedy is not one silver bullet but a combination of policy, code, and operational preparedness.

Conclusion

WLFI/Dolomite wasn’t merely a headline about a token dump — it was a concentrated‑exposure stress test for DeFi primitives. Lenders, auditors, and risk teams should treat the episode as a practical case study: measure concentration, harden oracle and liquidation logic, and bake governance safeguards into the protocol lifecycle. With those measures, the same market shocks that hurt WLFI need not turn into systemic counterparty failures.

Sources

- World Liberty Financial borrows millions on Dolomite, defends WLFI collateral

- WLFI token dips 10% after World Liberty Financial defends $75M stablecoin loan

- Trump-linked WLFI erases $427 million token unlock proposal amid DeFi loan concerns

For wider context on market bellwethers and lending dynamics, see discussions on DeFi best practices and the underlying asset page for WLFI in our knowledge base.