Ripple/XRP as an Institutional Payments Play: Banks, Stablecoins, and Treasury Roadmap

Summary

Executive summary

Institutional treasuries and payments desks are rethinking settlement plumbing. For many, Ripple’s combination of the XRP Ledger, On-Demand Liquidity (ODL), and now native enterprise stablecoins presents a low-latency alternative to pre-funded nostro accounts and slow correspondent chains. More than 100 banks — including major institutions — are already running live pilots, and Ripple’s treasury-management roadmap signals a product approach geared to real-world corporate flows.

This article evaluates the bank pilots, the economics unlocked by USDC and RLUSD issuance on the XRP Ledger, the practical modules Ripple proposes for treasury management, and the regulatory context that explains why banks are experimenting now. It finishes with concrete commercial scenarios and a checklist treasury professionals can use when running pilots.

Why banks are piloting Ripple now

Banks test new settlement rails for three pragmatic reasons: cost, speed, and client demand. The current correspondent-banking model ties up capital in nostro/vostro accounts and produces reconciliation headaches. On-ledger settlement promises near-instant finality and a smaller operational footprint. Recent reporting that more than 100 banks are already testing Ripple in live pilots — including major institutions — is not hype; it reflects a cautious but practical move to reduce intraday liquidity and speed up cross-border flows (Coinpaper on Ripple bank pilots).

There’s also a regulatory and market-structure catalyst. Shifts in the U.S. regulatory conversation and clearer engagement from policy makers have reduced one big source of uncertainty, prompting pilot programs to accelerate rather than stall. Recent analysis shows Washington’s activity has materially altered the regulatory landscape for XRP and digital assets, encouraging institutional experimentation rather than paralysis (Blockonomi on regulation).

Who’s running pilots — a snapshot

Public reporting lists a broad mix of Tier 1 and regional banks participating in Ripple pilots. While some pilots are exploratory (proofs of concept), others are live corridor tests that move value between endpoints. Reported participants include global names such as Santander and large North American banks, alongside a set of correspondent banks and regional custodians. The scale and diversity of these pilots matter: they’re testing not just the protocol, but custody, KYC/AML flows, and the whole commercial plumbing required for bank-to-bank settlement (Coinpaper bank list).

These live tests typically fall into three categories:

- FX corridors where ODL reduces pre-funding needs.

- On-ledger stablecoin experiments for enterprise settlement.

- Intercompany and treasury netting pilots that explore reconciliation simplification.

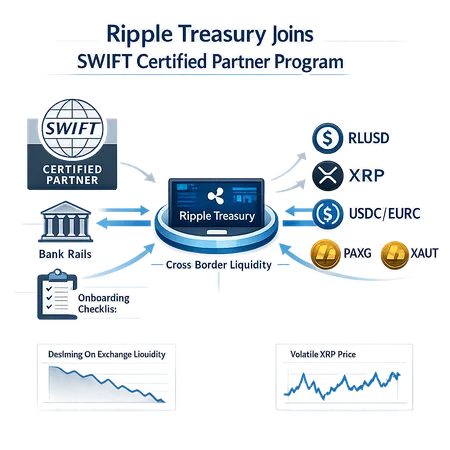

On-ledger enterprise stablecoins: USDC and RLUSD on the XRP Ledger

A turning point for institutional adoption is the presence of regulated, on-ledger stablecoins issued natively on the settlement ledger. USDC and RLUSD issued on the XRP Ledger change the settlement economics in important ways. A recent analysis canvasses how enterprise stablecoins on the XRP Ledger — specifically USDC and RLUSD — can lower friction and enable native settlement rails for corporate payments (Coinpaper on enterprise stablecoins).

Why does native issuance matter?

- Reduced FX and volatility exposure: A fiat-backed stablecoin removes the need to route value through a volatile bridge asset when the counterparty prefers stable units.

- Lower capital drag: Because stablecoins can be redeemed and settled natively, banks can reduce pre-funded nostro balances across corridors.

- Faster settlement and reconciliation: On-ledger tokens carry transaction metadata and immutable timestamps, improving automated reconciliation.

Compare two flows: the legacy corridor where Bank A prepays a nostro account at Bank B (days of capital tied up), versus an on-ledger stablecoin flow where a regulated issuer mints a token, transfers it on the XRP Ledger, and the recipient redeems with its custodian. The latter reduces intraday liquidity needs and shortens settlement finality from hours/days to minutes.

That said, issuance, custody, and redemption mechanics create new dependencies: issuer creditworthiness, reserve audits, custodian reliability, and on/off-ramp bandwidth. For treasury teams, these are not theoretical risks — they are operational constraints to model into liquidity stress tests.

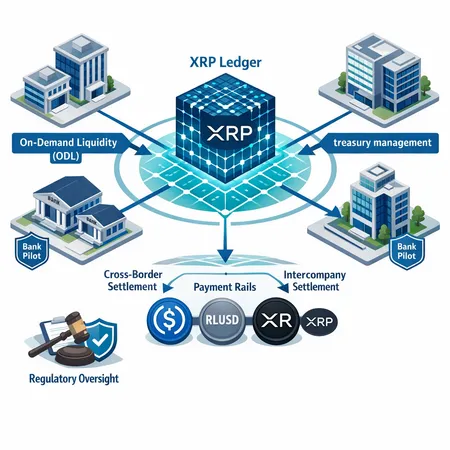

How On-Demand Liquidity (ODL) and stablecoins interact

ODL uses XRP as a bridge asset to source short-duration liquidity across corridors, dramatically cutting the need for pre-funded accounts. But volatility in XRP’s price exposes counterparties unless hedged. Enterprise stablecoins change the calculus: if both endpoints can accept a stablecoin on-ledger, the need to use XRP as a bridge declines. Instead of purchasing XRP, transactors can move USDC or RLUSD natively and redeem on the other side.

Practical implications:

- Where deep XRP liquidity exists and FX spreads are tight, ODL remains attractive for low-cost intraday FX.

- Where counterparty or regulatory preferences require fiat-denominated settlement, on-ledger stablecoins will often be favored.

- Hybrid architectures are likely: ODL for FX-intensive corridors, stablecoins for corporate payrolls, supplier payments, and liquidity-sensitive settlement.

Ripple’s treasury-management roadmap: modules and use cases

Ripple’s public roadmap and recent deep dives describe a modular treasury-management system designed for real-world corporate and bank flows. The architecture envisages distinct modules for liquidity orchestration, FX routing, compliance screening, and settlement finality: a practical toolkit for treasury teams rather than a single monolithic product (ZyCrypto on Ripple’s treasury system).

Core modules and practical use cases:

Liquidity management and orchestration: Dynamic sourcing of liquidity from custodians, exchanges, or on-ledger stablecoin pools to minimize cost and maximize speed. Use case: a bank auto-selects the least-cost path between pre-funded nostro, ODL, or USDC on-ledger for each payment.

FX routing and smart rails: Automated selection between direct fiat rails, XRP bridge, and stablecoin transfers based on price, speed, and compliance constraints. Use case: routing payroll payments in a multi-currency payroll run to minimize FX slippage.

Compliance and counterparty screening layer: Embedded KYC/AML checks and transaction screening to satisfy bank controls while preserving settlement speed. Use case: pre-flight checks that reject or route a payment differently if compliance flags arise.

Intercompany netting and multilateral settlement: Net positions across subsidiaries on-ledger to reduce gross payment volumes. Use case: multinational corporates using on-ledger netting to compress intra-group flows at month-end.

Reporting, audit, and reconciliation tools: Chain-native data used to generate audit trails and automate reconciliation with treasury systems. Use case: automatic exception reports that match ledger transactions to ERP invoices.

These modules are practical: treasury teams evaluate them not by feature lists but by how they change day-to-day metrics — capital tied up, failed payment rates, FX cost, and reconciliation headcount.

Regulatory noise and why experimentation continues

Cryptocurrency regulation has been noisy, and for good reason: custody, issuer reserves, and market conduct require careful oversight. Yet the regulatory conversation has evolved; a recent analysis suggests that policy activity in Washington has reshaped the dialogue around XRP and institutional digital assets, creating a more navigable environment for banks to pilot (Blockonomi regulatory piece).

Key regulatory considerations for banks and corporates:

Token classification and issuer obligations: Stablecoin issuers must demonstrate reserve practices, redemption rights, and transparency.

Custody and custody-provider scrutiny: Banks will rely on regulated custodians or trust arrangements for fiat-backed tokens.

AML/CFT and sanctions screening: On-ledger transactions are transparent but require robust screening and privacy-respecting workflows.

Prudential capital and liquidity rules: Regulators may update how on-ledger exposures are treated for capital purposes; pilots help banks model regulatory impacts.

Regulatory clarity is improving but not uniform across jurisdictions. That unevenness is part of why banks run pilots: to gather jurisdiction-specific evidence, demonstrate controls, and engage regulators with real data.

Commercial scenarios where Ripple and on-ledger stablecoins make sense

Cross-border supplier payments—SME to large corporate: A corporate treasury paying a supplier in a small FX corridor can reduce cost and speed using a native stablecoin transfer and instant redemption at the supplier’s custodian, eliminating days of nostro reconciliation.

Intercompany netting and cash concentration: Multinationals can net regional payables and receivables on-ledger and settle net positions in USDC or RLUSD, reducing intra-group FX churn and bank fees.

Low-value high-frequency remittances: Remittance providers and banks can combine ODL where XRP liquidity is favorable with stablecoins for on-ramp/off-ramp consistency to cut settlement time and fees.

Time-critical FX settlement: Trading desks needing same-day certainty use ODL for FX execution when latency matters, while corporates that prioritize currency stability choose on-ledger stablecoins.

Treasury liquidity pooling and sweeps: Banks can offer corporates pooled liquidity products where excess cash is tokenized on-ledger and moved to central treasury pools instantly.

Practical checklist for treasury and payments teams running pilots

- Define KPIs: settlement time, failed payment rate, intraday liquidity reduction, reconciliation time, and total cost of execution.

- Map custody and redemption: who issues the stablecoin, where are reserves held, who redeems, and what is the SLA?

- Test compliance flows: integrate sanctions lists, KYC/AML screening, and automated exception handling.

- Model liquidity economics: run stress tests for FX moves, redemption runs, and counterparty default scenarios.

- Monitor operating controls: settlement finality, audit trails, and incident response.

- Engage regulators early: present pilot data and controls in jurisdictional briefings to reduce policy risk.

Platforms like Bitlet.app and others show how market infrastructure can integrate this functionality, but banks will want direct auditability and custody assurances before moving beyond pilots.

Risks and open questions

- Issuer risk: The stablecoin issuer’s reserve practices must be auditable and legally robust.

- Market liquidity: XRP or other on-ledger liquidity might be thin in some corridors, increasing cost or slippage.

- Legal settlement finality: Jurisdictions differ on whether ledger entries constitute final legal settlement.

None of these are showstoppers, but they matter to risk committees and compliance teams. Pilots are the right way to quantify them.

Conclusion

Ripple’s combination of the XRP Ledger, ODL, and native enterprise stablecoins like USDC and RLUSD presents a credible set of tools for banks and corporates to reengineer cross-border settlement. The technology reduces liquidity drag and speeds reconciliation, while the treasury-management roadmap targets the practical operational problems that treasuries face. Regulatory shifts and more than 100 live bank pilots show that adoption is no longer just theoretical — it’s an operational experiment being run in real corridors.

For treasury and payments professionals, the decision to pilot should be pragmatic: define clear KPIs, stress-test liquidity and issuer risk, and design compliance workflows that align with bank controls. The result could be materially lower operating cost and faster settlement — but only if treasury teams convert promising pilot data into repeatable, auditable production flows.

For many corporate and bank readers, investigating Ripple deployments alongside broader DeFi developments will be useful as ecosystem tooling and regulatory regimes evolve.

Sources

- Coinpaper — More than 100 banks are already testing Ripple (bank pilots)

- Coinpaper — USDC and RLUSD lead the pack as top enterprise stablecoins on the XRP Ledger

- ZyCrypto — Everything you should know about Ripple’s treasury management system

- Blockonomi — How ten days in Washington changed the regulatory landscape for XRP and digital assets