Ripple Treasury Joins SWIFT: What It Means for Bank Rails, RLUSD and XRP Liquidity

Summary

Snapshot: why this SWIFT move matters — and what it doesn’t

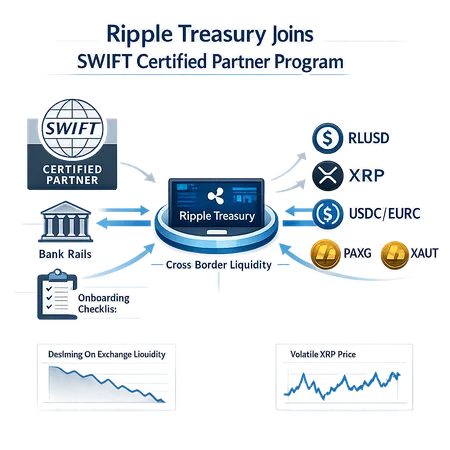

Ripple’s Treasury platform joining the SWIFT Certified Partner Program is a clear signal that Ripple wants to be treated as an operational peer to traditional payments vendors. Certification reduces one major form of friction: the technical and security checks banks use when evaluating third‑party connectivity. In practice, that makes it easier for banks to consider onboarding tokenized assets or stablecoins into existing payment flows — but it does not guarantee banks will immediately use RLUSD or XRP for large-value settlement.

Operational certification is a plumbing-level improvement: it helps with message formats, governance, secure connectivity and interoperability testing. Coinpedia’s write-up on the announcement captures this operational angle and the strategic optics of being closer to SWIFT’s ecosystem (Coinpedia).

What SWIFT certification implies operationally

Reduced integration overhead, not regulatory safe harbor

At a technical level, a SWIFT-certified partner typically complies with SWIFT’s connectivity standards, security expectations and testing regimes. For a bank evaluating a new counterparty, that translates to fewer technical unknowns and a shorter path from evaluation to sandbox testing. Banks that already use SWIFT’s messaging rails can map tokenized settlement flows to familiar operational patterns, for example pairing ISO 20022 messaging with token-transfer instructions.

But certification is not a regulatory endorsement. Banks will still run AML/KYC, sanction screening, custody due diligence, and legal reviews specific to digital assets. Institutional adoption depends as much on compliance tooling, custody guarantees and counterparty credit arrangements as on message interoperability.

Practical runbook improvements

- Faster sandboxing and interop tests with incumbent treasury teams.

- Clear expectations on message delivery, retries, and logging that match SWIFT norms.

- Easier accountability for incident response and auditing, since SWIFT certification implies certain operational controls are in place.

Those are meaningful for treasury operations that hate surprises. Still, the jump from sandbox to high-value, cross-border settlement requires robustness in liquidity, custody and legal contracts.

How Treasury + RLUSD could reshape bank rails (if the plumbing and liquidity cooperate)

Ripple’s Treasury platform is built to integrate tokenized assets and stablecoins into institutional workflows. Paired with RLUSD, the logic is straightforward: banks could use RLUSD as a programmable unit of account and settlement leg while continuing to route messaging via SWIFT-style processes. This creates three realistic use cases:

- Intrabank liquidity management and tokenized cash sweeps for corporate clients.

- Cross-border settlement corridors where RLUSD reduces FX hops or shortens liquidity chains.

- Tokenized asset liquidity—e.g., settling trades against tokenized gold (PAXG, XAUT) without routing through multiple fiat rails.

The latter is already being tested in the market: RLUSD gained tradable pairs like RLUSD/PAXG and RLUSD/XAUT on Bitrue, an example of product expansion into tokenized assets and a bridge between stablecoins and tokenized commodities (U.Today). That listing illustrates the potential for RLUSD to act as a settlement medium between tokenized instruments.

Why market liquidity still paints a mixed picture

Product integrations and SWIFT-level interoperability solve one class of problems. Liquidity and activity on exchanges and spot markets solve another — and those metrics matter to treasury desks.

Recent data show a worrying divergence: institutional‑grade product developments have accelerated on the corporate side, while retail and exchange liquidity for XRP have softened. For example, Binance liquidity indices for XRP hit a nine‑month low, suggesting thinner on‑exchange depth than markets expect for a settlement-grade asset (Finbold). Meanwhile, analysts warn that improving corporate credit metrics or regulatory progress doesn’t immunize the token from price downside if network activity weakens (FXEmpire).

Why does this matter? Banks and custodians look for predictable market depth when they accept an asset as settlement collateral. Thin order books increase slippage and make risk management more complex; they also raise concentration risks if a handful of venues provide most of the liquidity.

Stablecoin pairs help, but aren’t a silver bullet

Listing RLUSD pairs against tokenized gold (RLUSD/PAXG, RLUSD/XAUT) is a practical step toward composable rails. It allows market participants to express exposures without fiat on‑ramps. Yet pair listings on exchanges are just one piece of the liquidity puzzle — the real test is sustained volumes across multiple custodians, OTC desks, and regulated venues that institutional traders use.

In short: Treasury + RLUSD could reduce settlement friction, but banks will wait until liquidity and testing prove the rails can handle large ticket sizes without introducing outsized market impact.

Reconciling product momentum with market reality

There’s a familiar pattern in crypto enterprise adoption: product announcements and certifications create optionality and conversational entry points for banks, but operational adoption follows longer, corridor‑by‑corridor pilots. Ripple’s SWIFT certification does three practical things: shortens technical due diligence, provides auditability expected by banks, and positions RLUSD as a candidate for tokenized settlement. That said, the weak on‑exchange liquidity for XRP and cooling transaction counts suggest a multi‑year runway before widespread use.

FXEmpire’s coverage about corporate progress and lingering price risk encapsulates the tension: better institutional metrics (such as improving corporate ratings or partnerships) help the commercial case, but they don’t immediately fix market‑microstructure problems that matter for settlement.

Realistic timelines and phases for adoption

What should institutional and TradFi practitioners expect? A conservative pacing model looks like this:

- 0–12 months: Integration pilots and sandboxing with select correspondent banks and custodians. Emphasis on compliance, message mapping, and legal frameworks. RLUSD used in limited, controlled transactions and internal liquidity management.

- 12–24 months: Corridor pilots extend to tokenized assets (e.g., PAXG/XAUT pairs) and OTC desks begin supporting bigger notional trades. Some regulated venues may offer RLUSD pairs; market‑making commitments could be contracted.

- 24–36+ months: If liquidity deepens, custodians and banks may offer RLUSD as part of FX hedging and settlement toolkits in specific corridors. Broader adoption will still depend on macro stability, regulatory clarity and competing rails (CBDCs, traditional FX nets).

This timeline is intentionally cautious. Banks move slowly; they demand crystal-clear custody, insurance and regulatory comfort before routing client funds through new rails.

What institutional practitioners should monitor now

- Liquidity depth across venues for XRP and RLUSD, not just headline listings. Track spreads, book depth and who the market makers are.

- Custody commitments and insurance terms offered by prime custodians for RLUSD and tokenized assets.

- Legal and settlement finality: whether counterparty agreements recognize on‑chain settlement events and how reversals / disputes are handled.

- Corridor pilots and correspondent bank participation. The list of banks willing to run node or custody services is a strong signal.

- Competing initiatives: CBDC pilots and large banks’ tokenization projects that could reduce RLUSD’s addressable use cases.

Platforms like Bitlet.app and institutional data providers can help teams track these metrics in real time — but teams should combine on‑chain, on‑book and OTC intelligence to get the full picture.

Bottom line

Ripple’s entry into the SWIFT Certified Partner Program via its Treasury platform is an important operational milestone: it narrows integration friction and makes the conversation with banks more straightforward. Paired with RLUSD and emergent stablecoin pairs (RLUSD/PAXG, RLUSD/XAUT), there is a credible path to tokenized settlement in niche corridors.

However, institutional adoption requires more than integration checkboxes. Robust, multi‑venue liquidity and sustained transaction activity are the gating factors — and current data on XRP liquidity and network engagement are a sobering reminder that product progress on one axis doesn’t automatically translate to settlement‑grade readiness on another. Expect measured pilots in the near term and corridor-specific adoption over the next 1–3 years, with broader scale contingent on liquidity improvements, regulatory clarity, and proven custody frameworks.

For practitioners evaluating this evolution, focus on operational readiness (message mapping, custody, legal finality) and market readiness (deep, diversified liquidity and market maker commitments) rather than announcements alone.

Sources

- Coinpedia — Ripple expands into SWIFT system with Treasury platform: https://coinpedia.org/news/ripple-expands-into-swift-system-with-treasury-platform/

- U.Today — RLUSD secures listing against tokenized gold (RLUSD/PAXG, RLUSD/XAUT): https://u.today/ripple-usd-stablecoin-secures-rare-listing-against-tokenized-gold-by-tether-and-paxos?utm_source=snapi

- FXEmpire — Ripple scores BBB rating but price risks remain: https://www.fxempire.com/forecasts/article/xrp-news-today-ripple-scores-bbb-rating-but-price-risks-40-drop-1589552

- Finbold — XRP liquidity index on Binance crashes to a 9‑month low: https://finbold.com/xrp-liquidity-index-on-binance-crashes-to-a-9-month-low/?utm_source=snapi

For related market context, many teams still benchmark tokenized rails against incumbent rails and DeFi experiments, while macro hedging often uses reference assets like Bitcoin for cross‑asset comparisons.