Metaplanet’s 5,075 BTC Buy and the New Shape of Corporate Bitcoin Treasuries

Summary

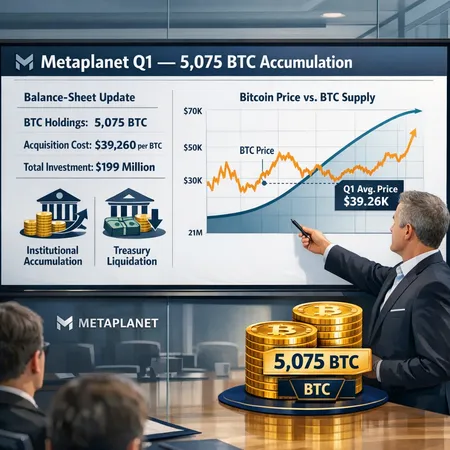

Snapshot: Metaplanet’s Q1 Accumulation and Why It Matters

Metaplanet disclosed a Q1 purchase of 5,075 BTC, taking its publicly reported holdings to 40,177 BTC. That scale places the company among the world’s largest corporate holders and anchors a conversation about how public companies are using crypto on their balance sheets. Reports that detail the buy and Metaplanet’s broader objectives are available in industry coverage such as The Block and Blockonomi, which also note acquisition price context and the firm’s stated ambition for as much as 100,000 BTC in time. For market-watchers, this isn’t just a PR headline—it's a data point about concentrated demand and the evolving structure of corporate treasury strategies.

A quick read of the numbers

Metaplanet’s accumulation was not a marginal purchase. When a single public company sizes a treasury position in the tens of thousands of BTC, its decisions affect perceived scarcity, counterparties’ hedging, and how other corporates think about allocation. Cointelegraph and other outlets outlined the Q1 purchases and color around how these buys were executed across OTC desks and options markets, a reminder that tactical choice matters as much as headline quantity.

Why companies like Metaplanet buy Bitcoin: motives and mandate

Corporate motivations for holding BTC vary but cluster around a few repeatable rationales:

- Inflation and currency hedging: For firms with large cash piles, BTC is sometimes framed as a non-sovereign store of value.

- Strategic optionality and business integration: Treasuries can support future product plans (custody partnerships, tokenized offerings) or signal alignment with crypto-native customer segments.

- Return enhancement: Companies may view BTC as an asymmetric return asset with long-term upside, versus near-zero yields on cash.

- Balance-sheet diversification and signaling: Large BTC positions provide a signaling effect to markets and can align management with long-term, risk-seeking investors.

These motives matter because they determine how a firm treats BTC on its books—long-term strategic reserve versus a liquid trading asset—and that treatment drives selling behavior (or lack of it) during stress.

Acquisition price, valuation math, and balance-sheet treatment

Public reporting around Metaplanet’s add disclosed an acquisition price range and helped analysts model mark-to-market exposure. Blockonomi summarized the purchase price and the firm’s long-term 100k BTC aspiration, providing context for implied dollar-weighted cost bases. For CFOs, the two most important balance-sheet questions are:

- How is Bitcoin classified—cash equivalent, intangible asset, or inventory? Classification dictates accounting volatility and impairment rules.

- What is the dollar cost basis and how large is unrealized P&L relative to equity? A concentrated BTC position can materially swing reported equity with price moves.

Simple balance-sheet math: if Metaplanet holds 40,177 BTC and its dollar-weighted acquisition price is X, then a 10% move in BTC price generates (~40,177 * current price * 10%) change in enterprise value attributable to that line item. The leverage effect on reported equity increases when the firm’s non-BTC capital base is modest. CFOs must project scenarios (downside stress multiples, impairment thresholds) and set policy triggers for review or rebalancing.

Comparing Metaplanet to other public treasuries

Metaplanet’s 40k+ BTC sits behind a very small group of corporate treasuries by size. The addition of 5,075 BTC in a single quarter put Metaplanet ahead of many public companies and behind the largest holders, a dynamic noted in industry reporting. These concentrated corporate holders are no longer niche: their aggregate decisions are a meaningful component of net available supply.

But companies differ in intent and tolerance. Some hold passively with long-dated intent; others actively trade or use derivatives to hedge exposures. That heterogeneity matters when forecasting whether corporate holdings are sticky or likely to be sold in stress.

Is the corporate treasury boom bifurcating? Accumulation vs. liquidation

There’s growing evidence of a split: a set of selective, conviction-led accumulators (Metaplanet among them) and a separate cohort that may opportunistically liquidate. Recent coverage highlights that some firms and governments have begun to sell reserves, unwinding past accumulation cycles; CoinDesk has tracked that treasury unwind trend, signaling the market cannot assume perpetual net corporate accumulation.

Why bifurcation emerges: firms have different mandates, liquidity needs, and governance. Accumulators tend to:

- Have dedicated crypto policy committees, ample free cash, and long-term revenue optionality tied to crypto ecosystems.

- Treat BTC as a strategic reserve and accept volatility on the balance sheet.

Liquidators tend to:

- Face cash needs, regulatory or tax shocks, or a governance reassessment; or

- Be constrained by accounting and capital market signaling that make realized gains attractive to return to shareholders.

This bifurcation shapes market structure: concentrated accumulation reduces available float and can raise price sensitivity to sell flows, while opportunistic liquidation creates episodic supply shocks.

Market impact: price impact of concentrated corporate buyers and sellers

When large corporates buy, they typically transact OTC or via derivatives to minimize slippage—but they still remove coins from the free float, tightening on-chain supply metrics. The visible price impact is not only the trade itself: it is the signaling effect that other market participants interpret. A large buy can trigger momentum inflows from funds and retail. Conversely, a large sell—particularly if unexpected—can cascade through funding markets and derivatives, amplifying price moves.

Priced impact depends on liquidity depth, execution method, and market sentiment. For firms executing large purchases, staggered OTC buys, options-driven position construction, and limit-based programs can dampen immediate price effects but may stretch signaling across quarters. Cointelegraph’s reporting on Metaplanet’s use of options markets underscores that execution choice influences both cash outlays and tail risk exposure.

Scenarios for supply-side pressure (what CFOs and allocators should model)

Modeling supply stress is about scenario-building:

Scenario A — Sticky Accumulation: Large corporates continue to accumulate selectively. Result: structural tightening of available supply, higher realized volatility but bullish skew. Price regime favors long-dated option exposure and strategic treasury holdings.

Scenario B — Opportunistic Liquidation: Some treasuries sell into rallies to realize gains or cover cash needs. Result: episodic supply shocks, heightened short-term volatility; funds increase hedging costs, and premium in options markets rises. CoinDesk’s reporting that some corporates and governments are selling supports this risk.

Scenario C — Rotation and Hedged Exposure: Corporates keep BTC but use collars or futures to limit downside, transferring tail risk to markets. This increases derivatives activity and can mute on-chain supply moves while raising counterparty concentrations.

For each scenario, CFOs should quantify: cash-flow buffers required to avoid forced liquidation, mark-to-market sensitivity to a range of prices, and haircut assumptions for borrowing against BTC. Institutional allocators should overlay correlation matrices (BTC vs. FX, rates, equities) to evaluate portfolio level hedges and rebalancing triggers.

Practical checklist for treasury teams

- Define policy: allocation limit (percent of total assets), rebalancing triggers, and permitted instruments (spot, OTC, options, futures).

- Stress-test: simulate 25/50/75% price declines and model liquidity needs and covenant breaches.

- Execution plan: preferred counterparties, staging windows, and whether to use options to smooth exposure.

- Disclosure and governance: prepare investor communications and board-level sign-off processes.

- Monitor market structure: its not only price but available liquidity—watch on-chain supply metrics and OTC desk depth.

Bitlet.app and other platforms are part of the evolving infrastructure that treasuries will use for execution and custody; understanding the ecosystem helps in choosing partners.

Takeaway for CFOs, allocators, and strategists

Metaplanet’s 5,075 BTC add is both a market event and a lens: it shows how large corporates can materially influence perceived scarcity while also highlighting that not all treasuries behave the same. The corporate landscape appears to be bifurcating: a set of conviction-led accumulators versus a group likely to realize gains when pragmatic considerations demand. For decision-makers, the focus should be on clear policy, conservative stress-testing, and execution discipline—because concentrated flows, not just headline amounts, drive short- and medium-term market dynamics.

Sources

- Metaplanet adds 5,075 BTC, The Block: https://www.theblock.co/post/396190/metaplanet-adds-5075-bitcoin-bringing-total-holdings-to-40177-btc-to-become-third-largest-among-public-companies

- Blockonomi coverage of Metaplanet’s holdings and price context: https://blockonomi.com/metaplanet-reaches-40177-bitcoin-becomes-third-largest-corporate-btc-holder-globally/

- The Bitcoin treasury boom is unwinding (some sell), CoinDesk: https://www.coindesk.com/business/2026/04/02/the-bitcoin-treasury-boom-is-unwinding-as-some-companies-and-governments-sell-holdings

- Cointelegraph on Metaplanet’s Q1 purchases and options use: https://cointelegraph.com/news/metaplanet-adds-5-075-btc-in-q1-bitcoin-options?utm_source=rss_feed&utm_medium=rss&utm_campaign=rss_partner_inbound

For readers who want a primer on market bellwethers, remember that Bitcoin often leads crypto risk-on moves, and DeFi-derived liquidity serves as an alternate channel for large participants—see more on DeFi when modeling derivatives and lending exposures.