What Coinbase’s Altcoin-Backed Loans Mean for Borrowers, Markets and Liquidity

Summary

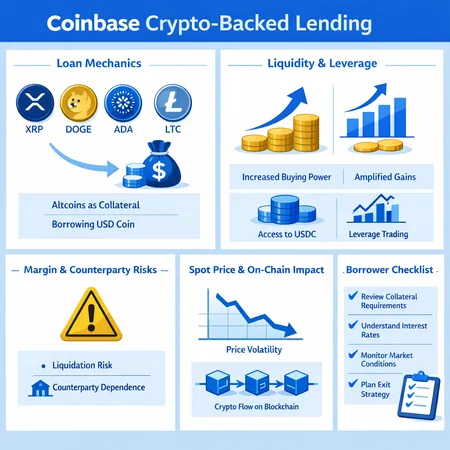

The headline: what Coinbase added and how the $100k USDC loan works

In short, Coinbase expanded its U.S. crypto-backed lending product to accept XRP, DOGE, ADA and LTC as collateral and is offering USDC loans up to $100,000 against those assets. The product lets qualified borrowers pledge supported altcoins and borrow USDC, with collateral-to-loan mechanics and liquidation rules that determine how much you can safely borrow. Coinbase’s announcements and coverage provide the basic terms and the expansion details — see the official reporting at ZyCrypto and Coinpedia for the launch specifics and the $100k loan mechanics.

The practical mechanics are familiar to anyone who’s used centralized crypto lending: you deposit collateral (XRP, DOGE, ADA or LTC), select a loan amount up to a maximum Loan-to-Value (LTV) threshold, and receive USDC. The loan is collateralized — if the collateral value falls enough relative to the loan, Coinbase can require additional collateral or liquidate holdings to cover the position. Coinpedia outlines the product cap and collateral mix, while ZyCrypto summarizes the expansion announcement and eligible assets.

How altcoin collateral works: LTV, liquidations and fees

At the core of any collateralized loan are three variables: the allowed LTV, the margin-call (or maintenance) threshold, and the liquidation penalty or fee. Coinbase hasn’t published every granular LTV schedule publicly in these articles, but the typical model looks like this:

- Initial LTV: a conservative fraction (for example, 40–70%) of your collateral’s value that determines the maximum borrowable USDC. Lower LTVs give larger price drawdown cushions.

- Maintenance threshold: a lower boundary that, when breached by collateral depreciation, triggers margin calls or automatic liquidation.

- Liquidation mechanics: forced sales or partial liquidation to restore the required collateral ratio, often with a fee or haircut.

Altcoins are more volatile than large-cap assets like BTC or ETH. That volatility translates to higher frequency of margin events and greater slippage at liquidation. For borrowers, this means actively managing positions (setting alerts, maintaining excess collateral) is essential. For lenders, higher volatility increases the operational burden of monitoring and the chance of under-collateralized shortfalls during rapid crashes.

Liquidity and leverage implications for XRP, DOGE, ADA and LTC markets

Allowing these altcoins as collateral lowers a practical barrier to using them as financing tools. That can produce several market effects:

- Increased spot liquidity into lending venues: Owners who previously held these coins for the long term may deposit them as collateral to access USDC liquidity without selling, increasing circulating supply on centralized platforms. That can concentrate supply on exchanges, making on-chain liquidity more exchange-centric.

- Greater leverage and derivative-like behavior: Borrowers can use the borrowed USDC to buy more of the same asset (or other assets), magnifying directional bets. This creates the possibility of feedback loops: price rises allow more borrowing and buying; price drops force liquidations and selling.

- Market depth and slippage: In less liquid markets (some XRP and DOGE trading pairs can be thin on certain venues), forced liquidations can produce outsized price moves. ADA and LTC have deeper markets, but sudden large liquidations still cause slippage.

- Interaction with DeFi: If borrowers move borrowed USDC into DeFi protocols for yield, the flows create additional demand for on-chain stablecoins and may increase protocol-level liquidity, but they also expose borrowers to smart-contract risk.

These dynamics make the market behavior for each token slightly different. DOGE—a memecoin with retail-driven flows—can see large swings from leveraged retail activity; XRP remains sensitive to regulatory news and concentrated holdings; ADA has protocol-driven fundamentals and staking flows that can buffer or amplify moves; LTC often tracks BTC sentiment but can be vulnerable to liquidity gaps.

Margin risk and counterparty risk: who bears what?

Lending platforms and borrowers each face distinct risks.

For borrowers:

- Liquidation risk: If collateral falls below the maintenance threshold, automatic or forced liquidation will realize losses irrespective of your long-term view.

- Basis and funding risk: You’re paying interest or fees (plus potential liquidation penalties) while exposed to collateral price moves.

- Operational risk: Mistakes in selecting LTV, not monitoring positions, or moving collateral off-platform can cause avoidable losses.

For Coinbase (the lender):

- Market risk: Sudden, correlated market crashes can devalue collateral faster than Coinbase can liquidate at sane prices, creating potential shortfalls.

- Concentration and counterparty risk: If a large percentage of loans are collateralized in a single altcoin, a melt-down in that asset concentrates risk.

- Custody and settlement risk: As a centralized lender, Coinbase assumes custody responsibilities. Mismanagement of reserves or failures in risk monitoring would create platform-level exposure.

Counterparty risk is particularly salient because centralized lending is not the same as on-chain overcollateralized lending. Borrowers trade custody for credit access; the lender is responsible for managing liquidation windows, spreads and execution quality when selling collateral. As such, platform governance and transparency become risk mitigants to watch.

How broader adoption of altcoin-backed loans could affect spot prices and on-chain flows

Widespread use of altcoin-backed loans would shift both behavior and liquidity patterns:

- Exchange inflows: Collateral is typically held on-platform. Higher deposits can mean larger exchange balances for these tokens, which historically correlates with selling pressure risk.

- Stablecoin demand: Borrowers taking USDC increase demand for stablecoins, tightening stablecoin markets and potentially driving capital into yield-bearing uses.

- On-chain withdrawals vs exchange-held collateral: Borrowers who want to keep collateral decentralized may use wrapped or bridged strategies, increasing cross-chain flows.

- Price impact through liquidation cascades: Chains of leveraged positions can amplify price movements. A forced sale in XRP could depress prices across venues, prompting more liquidations and selling in a domino effect.

There is also an equilibrium effect: if borrowing against an asset becomes commonplace, market participants will price in that additional liquidity source — buyers may demand a premium for liquid coins held off-exchange, and markets could become more sensitive to lending conditions and margin-rate changes.

Practical borrower checklist: how to use altcoin-backed loans prudently

Use this checklist before pledging XRP, DOGE, ADA or LTC as collateral:

- Know the LTV and maintenance thresholds. Run stress tests: what happens if the collateral drops 30%? 50%?

- Keep a buffer. Maintain extra collateral or a stablecoin reserve to top up positions during volatility.

- Understand liquidation mechanics and fees. Read the fine print: how quickly will Coinbase liquidate, and what penalties apply?

- Avoid reinvesting borrowed USDC into the same asset unless you can tolerate a leveraged long and its asymmetric risk.

- Monitor concentration risk. Don’t collateralize multiple loans with the same underlying exposure across venues; diversification matters.

- Factor in custody and counterparty exposure. If you need access to the private keys for safety, centralized lending may not be ideal.

- Consider timelines: short-term liquidity needs (e.g., paying bills, seizing an arbitrage) differ from longer-term leverage plays.

- Use alerts and automation. Price alerts and automated top-ups reduce the chance of surprise liquidations.

- Shop for execution: if liquidation is likely, know where Coinbase will route sales and what slippage to expect.

- Read tax and regulatory implications. Borrowing against crypto can have taxable or reporting implications depending on jurisdiction.

This is a product category where tools like Bitlet.app that focus on structured crypto financial services can help users compare options and price risk, but always perform your own due diligence.

Final perspective: expansion is useful — but risk matters

Accepting XRP, DOGE, ADA and LTC as collateral expands market access: more holders can unlock USD-pegged liquidity without immediate tax events or forced selling. That’s useful for personal liquidity management, trading strategies, or DeFi composability. But the same features that make altcoin collateral appealing — accessibility, retail supply, protocol utility — also make them more volatile and prone to concentrated sell events.

For advanced retail borrowers, the decision to use altcoin-backed loans should be tactical and accompanied by active risk management. Understand the exact LTVs, liquidation windows and platform rules; assume volatility; and maintain buffers. If used thoughtfully, these products provide useful liquidity. If used recklessly, they can amplify losses quickly.

For many traders, Bitcoin still serves as the primary barometer of risk-on and risk-off regimes, but adding altcoin-backed lending into the toolbox will make XRP, DOGE, ADA and LTC more intertwined with credit dynamics going forward.

Sources

- Coinbase expands its crypto-backed lending product to XRP, DOGE and Cardano: Coinbase expands its crypto-backed lending product to XRP, DOGE and Cardano (ZyCrypto)

- Details on the $100k USDC loans backed by XRP, DOGE, ADA, LTC: Coinbase launches $100k USDC loans backed by XRP, DOGE, ADA, LTC (Coinpedia)