Stress‑Testing Bitcoin: Geopolitical Shocks, Retail Exodus, and Portfolio Rules for Tail Risk

Summary

Introduction: Why the fragility narrative matters now

For macro traders and portfolio managers, fragility is not an abstract idea—it’s a set of observable signals that change how you size positions, hedge, and stress‑test portfolios. In the past month Bitcoin’s drawdown found a focal point in renewed geopolitical headlines. That alone wouldn’t be unique; what makes the current episode noteworthy is the simultaneous weakening of retail demand and emerging evidence that long‑term holders are distributing into the selloff. Those three vectors—headline risk, retail outflows, and holder selling—combine to increase the probability of violent price moves and make conventional volatility estimates unreliable.

Geopolitical shocks: headlines as a volatility amplifier

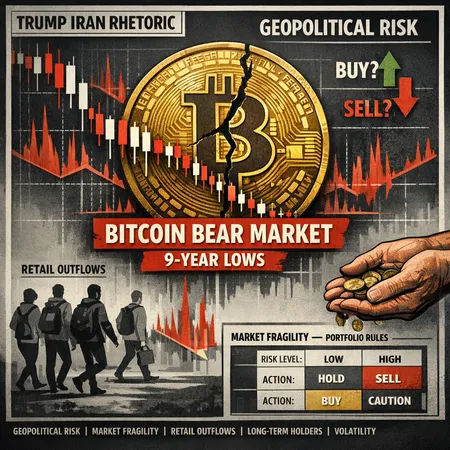

Market participants reacted to sharp headlines tied to President Trump’s escalatory rhetoric toward Iran, and Bitcoin’s low in 2026 coincided with intensifying geopolitical fear. Reporting from Unchained Crypto links the 2026 low to that rhetoric and the broader risk‑off tone that swept markets (Unchained Crypto).

Geopolitical risk behaves like a stochastic shock: it can be rare but high‑impact, and it interacts with liquidity conditions to amplify moves. When large, simple narrative shifts occur—war talk, sanctions, or unexpected military escalations—risk assets and safe havens reprice quickly. For BTC specifically, headlines can switch sentiment rapidly because the market structure is still partially retail dominated and liquidity is uneven across venues.

Retail outflows: a weak bid beneath price

Exchange flow analysis shows retail activity on major platforms has slumped. Blockonomi highlights that retail inflows on Binance have fallen to levels not seen in nine years, suggesting retail demand is materially weaker at current prices (Blockonomi).

Why does this matter? Retail provides a base of liquidity that can absorb order flow in normal times. When retail participation dries up:

- Depth evaporates at key price levels.

- Market orders (panic sells or momentum buys) move price more than they used to.

- Bid‑ask spreads widen on thinner venues, increasing slippage for large trades.

For portfolio managers, weak retail inflows mean you cannot assume restored retail liquidity will prop prices during a shock. That changes sizing: the same notional bet now implies a larger market impact risk.

Long‑term holders: distribution evidence and supply stress

Long‑term holders (LTHs) historically act as a stabilizing force—they sell sparingly and only after significant price appreciation. Recent coverage points to LTH distribution as unrealized losses mount, with some long‑dated holders choosing to cut exposure rather than ride out the drawdown (Cointribune).

When LTHs shift from accumulation to distribution, the net supply curve tilts from inelastic to elastic: more coins become available at lower prices. Combine that with retail outflows and headline risk, and you have a recipe for a deeper, faster correction.

Contrarian price scenarios and tail risks

Market commentary has started to include severe downside scenarios. A Bloomberg strategist outlined a case for a much lower Bitcoin price in a stressed macro environment, arguing downside paths back toward historical support are plausible (NewsBTC links to Bloomberg commentary). These forecasts are useful not because they’re guaranteed to happen but because they quantify tail risk that many models ignore.

Build scenario buckets that are explicit and repeatable:

- Scenario A (Idiosyncratic correction): 20–35% drawdown from current price, quick rebound in 3–6 months.

- Scenario B (Protracted bear): 35–65% drawdown, weak retail and LTH liquidation prolong recovery 12–24 months.

- Scenario C (Tail event): 65%+ drawdown, triggered by severe macro shock or systemic liquidity freeze—analogous to 2008-like deleveraging.

These buckets should map to rule‑based portfolio actions (hedging, de‑risks, or opportunistic rebalancing) rather than ad‑hoc calls.

Portfolio frameworks: sizing, hedges, and volatility budgets

Below are practical, scenario‑driven rules for firms building stress‑tested crypto allocations.

1) Volatility budget and dynamic sizing

- Define a portfolio volatility budget for crypto (e.g., 3–7% of total portfolio volatility). Use realized and implied vol to set initial sizing.

- Scale positions inversely with realized liquidity metrics: if exchange depth at -1% moves is below X BTC, reduce size by Y%. This accounts for market impact in thin conditions.

2) Tail hedging ladder

- Layered protection: buy cheap puts or put spreads at multiple strikes rather than a single hedge point. For example, 25% protection at -25% strike, 15% at -40%, and 10% at -60%.

- Time-stagger hedges so you don’t pay premium on the entire protection horizon. Reassess cadence monthly or on major geopolitical events.

3) Liquidity tranching and staggered entries

- Allocate exposure across tranches capitalized for different scenarios: dry‑powder tranche (cash reserve), tactical tranche (opportunistic buys), and carry tranche (yield strategies). This reduces the risk of being fully committed when liquidity gaps widen.

4) Event‑triggered rules

- Predefine triggers based on observable metrics: sustained retail outflows (e.g., retail inflows below 50% of 12‑month average for 4 weeks), LTH supply increase above a threshold, or headline risk score above X from a news aggregator.

- When triggers fire, automatically tighten sizing by a fixed percent and increase hedge notional.

5) Stress tests and Monte Carlo with non‑normal shocks

- Run stress tests that randomly inject headline shocks (large negative jumps) correlated with liquidity drawdowns. Use heavy‑tailed distributions to model returns rather than Gaussians.

- Simulate market impact for trade sizes using real depth curves from several exchanges to estimate slippage costs.

Implementation: practical steps for trading desks

Instrument coverage: ensure access to on‑exchange futures, OTC liquidity, and options for layered hedging. Liquidity fragmentation matters—use venues that can source block fills.

Operational rules: set preauthorized adjustments (e.g., reduce exposure X% if retail inflows drop below threshold) to avoid delayed human decision‑making during fast declines.

Reporting: include crypto stress metrics in portfolio risk dashboards—retail inflow rate, LTH supply change, liquidity at bid‑1% and ask+1%, and a headline risk index.

Counterparty and custody: evaluate counterparty concentration; in tail events, settlement and custody frictions can be the final failure point. Platforms like Bitlet.app are part of a broader ecosystem you might use for execution or settlement, but always vet settlement risk carefully.

Conclusion: fragility is a feature, not a bug

Current data—geopolitical flareups, retail outflow signals, and LTH distribution—paint a coherent fragility narrative. Treat it as actionable intelligence: encode scenarios, budget volatility, stagger entries, and put layered hedges in place. That way you preserve optionality and avoid being forced sellers in a low‑liquidity environment.

For macro traders and portfolio managers, the choice is clear: either accept higher realized drawdowns or pay for disciplined, repeatable insurance in advance.

Sources

- Unchained Crypto — Bitcoin hits 2026 low as Trump escalates Iran war rhetoric

- Blockonomi — Bitcoin retail activity hits 9‑year low

- Cointribune — Long‑term holders begin to sell

- NewsBTC (Bloomberg strategist coverage) — New Bitcoin crash ahead forecast

For many institutional readers, Bitcoin remains the primary crypto risk exposure, while alternatives and yield strategies on DeFi can serve as tactical tranches—but only when their liquidity and counterparty risk are fully modeled.