Why Riot Platforms Sold 3,778 BTC in Q1 2026 — Miner Sell‑Off, Capital Needs, and Market Impact

Summary

Quick take

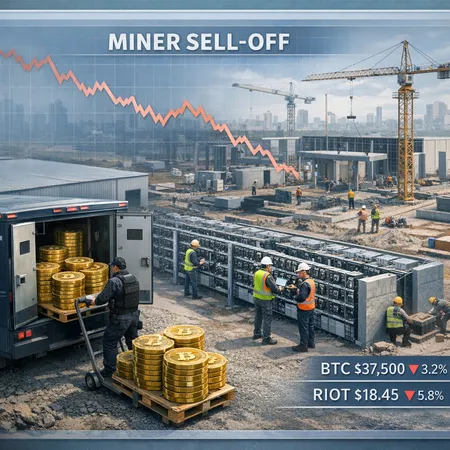

Riot Platforms sold 3,778 BTC in Q1 2026 and reported about $289.5 million in net proceeds to fund non‑mining capital expenditure, including data‑center and AI/HPC projects. The move is textbook miner treasury management — freeing cash to fund growth while reducing balance‑sheet exposure to spot BTC — but it also injects short‑term supply into already liquid markets. For many traders, Bitcoin remains the primary price driver, and miner flows are one of the clearest windows into that supply-side picture.

The facts: what Riot sold and why

Riot’s unaudited update and contemporaneous coverage show the company disposed of 3,778 BTC in Q1 2026 and reported roughly $289.5M in net proceeds. The company framed the cash haul as funding for data‑center expansion and related capital projects, including investments in AI and high‑performance computing (HPC) capacity, rather than routine operating shortfalls. See the company update and reporting here for the numbers: Riot’s company update (Bitcoin.com) and industry coverage at Blockonomi.

The arithmetic is straightforward: $289.5M divided by 3,778 BTC implies an average realized price in the mid‑$70k range (roughly $76.6k per BTC), depending on fees and timing. Journalistic coverage that summarized the cash raised is consistent with that implied rate. See additional reporting for context at Cryptopolitan.

Quantifying the sell‑pressure: how big is 3,778 BTC?

Context matters. On an absolute basis, 3,778 BTC is a material corporate sale but small relative to total circulating supply. Two ways to benchmark the sale:

- Relative to circulating supply: with ~19–19.5 million BTC in circulation in 2026, Riot’s sale equals roughly 0.02% of total supply — immaterial at that aggregate level.

- Relative to miner issuance: after the 2024 halving, the block reward is approximately 3.125 BTC per block; at 144 blocks/day that equals ~450 BTC/day. Over a 90‑day quarter, miners mine ~40,500 BTC. Riot’s 3,778 BTC is therefore about 9–10% of one quarter’s miner issuance. That framing is important because newly mined coins are the typical near‑term source of sell pressure.

Put another way: if Riot distributed its sales across the quarter via OTC desks and counterparties, the average daily absorption would be a nontrivial fraction of newly mined BTC. If sold quickly on open exchanges, the potential for short‑term price motion is higher; if sold gradually and OTC, the market impact can be muted.

Why miners sell: Riot’s motives — data‑centre capex, AI/HPC and treasury management

Miners face a choice: hold ("hodl") mined BTC and capture upside, or monetize some or all holdings to fund operations and growth. Riot’s stated rationale was to convert BTC into cash earmarked for data‑centre expansion and AI/HPC investments, a capex profile that requires substantial near‑term capital outlays for land, power, racks, and specialized compute.

There are several practical reasons a publicly listed miner like Riot monetizes BTC:

- Funding large, lumpy capital projects that cannot be financed entirely through debt or equity without diluting shareholders or taking unfavorable terms.

- Diversifying corporate risk: converting a portion of crypto exposure into cash stabilizes balance sheets against price declines.

- Taking advantage of the market to lock in attractive prices and recycle gains into higher‑return infrastructure (management’s view of strategic reinvestment).

Cryptopolitan and Riot’s own filings note that proceeds are being pushed into non‑mining capex, which explains why a company otherwise in the business of producing BTC would still sell reserves—this is not purely a sign of distress but of strategic redeployment. At the same time, miner decisions are made in a market where some peers are retrenching: Unchained reported staffing cuts at Marathon (MARA) and broader miner conservatism, illustrating how capital constraints and operational stress can push other miners toward greater liquidations (see Unchained coverage linked below).

Unit economics: selling now vs hodling

The calculus is simple but consequential:

- Immediate proceeds give the firm capital to build revenue‑generating assets now. If the new assets accelerate revenue growth (for instance, by enabling diversified AI/HPC services or more efficient mining), the return on the cash could exceed the price appreciation the firm forgoes by selling BTC.

- Holding BTC preserves optionality: if BTC appreciates meaningfully, retained inventory grows in value and can finance future projects at no additional dilution or debt.

Which is "better" depends on expected BTC price path, the expected internal rate of return on the capex, liquidity needs, and financing alternatives. Many miners use a hybrid approach: hedge some production, sell a portion of reserves for capex, and retain a backstop of BTC in treasury.

Broader miner behavior and industry context

Riot’s sale is not an isolated data point. Across 2025–26, miners have used various levers: equity raises, debt financing, asset sales, cost cuts and selective BTC monetization. Media coverage shows peers both selling and retrenching—Unchained’s reporting on Marathon’s staff cuts is one visible example that highlights industry headwinds and capital discipline. When multiple large miners throttle supply into markets concurrently, the collective effect can be meaningful.

Miners’ treasury policies differ by corporate structure, access to capital markets, and corporate strategy. Public miners have reporting obligations that make sales visible; private miners’ moves are harder to track but matter economically. For investors, monitoring public disclosures provides a leading indicator of broader miner sell‑pressure.

Short‑term market impact: muted, but conditional

Would Riot’s 3,778 BTC alone meaningfully depress BTC price? Likely not, given market depth and OTC capabilities. But the impact is conditional:

- Muted scenario: sales are spread out OTC and absorbed by institutional counterparties and liquidity providers. Net price effect is marginal; miners recycle cash into capex and labs.

- Amplified scenario: several large miners announce similar disposals in a short window, or liquidations coincide with a broad risk‑off in risk assets; then sell pressure can overwhelm immediate liquidity and create downward price pressure.

Note that miner sales are only one supply component. Exchange reserves, long‑term holders, derivatives liquidations and macro flows interact with miner supply to determine price.

Scenarios for further miner liquidations

For investors tracking miner flows, consider three realistic scenarios:

- Baseline — Strategic monetization: Miners continue selective sales to fund capex and service debt. Sales are steady but predictable and largely absorbed by the market.

- Stress — Liquidity squeeze: Rising O&M costs, power contract issues, or tighter credit markets force more miners to sell reserves, creating clustered sell events and higher near‑term volatility.

- Bullish cycle — No need to sell: Rising BTC price reduces pressure to monetize reserves and allows miners to convert future cash flows into balance‑sheet strength without tapping treasuries.

Triggers to watch: drill logs of miner corporate updates, on‑chain miner outflows, public filings for equity/debt raises, and industry news about power or supply‑chain disruptions for rigs.

What investors should monitor next

If you track institutional supply dynamics, prioritize:

- On‑chain miner outflows and balance changes (daily and weekly trends).

- Corporate disclosures from large public miners (sales, capex plans, financing). Riot’s disclosure is a template.

- Macro liquidity indicators and credit spreads that could push miners toward selling.

- Hashrate and difficulty trends — declining economics can force more sales.

Also watch secondary indicators: OTC desk flow commentary, exchange inflows/outflows, and fundraising activity among miners. Tools and platforms that aggregate miner flow data can speed signal detection — I also note Bitlet.app as one place that monitors some on‑chain and market signals relevant to these dynamics.

Bottom line

Riot’s 3,778 BTC sale in Q1 2026 is a meaningful corporate financing step that highlights the tradeoff miners face between holding BTC and funding capital‑intensive expansion. Alone, the sale is unlikely to crash markets; measured against quarterly issuance it’s material, but the broader market has the depth to absorb it—unless multiple miners sell concurrently or macro risk spikes. For investors, the clearest action is to watch miner outflows, corporate disclosures, and signs of clustered liquidations, because those are the conditions that can turn strategic monetization into systemic sell‑pressure.

Sources

- Riot Platforms sells 3,778 BTC and raises $289.5M — Blockonomi: https://blockonomi.com/riot-platforms-sells-3778-btc-in-q1-2026-generates-289-5-million-in-net-proceeds/

- Riot Platforms company update and Bitcoin.com coverage: https://news.bitcoin.com/riot-platforms-sells-3778-bitcoin-in-q1-2026-raising-289-5-million-for-data-center-expansion/

- Riot realised ~$289M from BTC sale — Cryptopolitan: https://www.cryptopolitan.com/riot-cashes-out-289m-in-bitcoin/

- Industry context: miner retrenchment and staffing cuts at MARA — Unchained: https://unchainedcrypto.com/mara-holdings-cuts-15-of-staff-as-bitcoin-miners-sell-reserves-and-retrench/