Christmas-week Bitcoin: how the year‑end options reset, ETF outflows, and institutional flows shape short‑term BTC risk

Summary

Executive snapshot

The Deribit year‑end reset (Dec. 22–24) has become a focal point for desks and treasuries this Christmas week. Market participants face three interacting forces: an outsized options expiry with a bullish put‑call skew, softening spot flows into ETFs, and elevated margin longs on exchanges — all overlaid by institutional signals of accumulation and liquidity clusters near $90K. Together, these dynamics create concentrated gamma, spot directional risk, and pockets of illiquidity that can amplify intraday moves.

For active traders and institutional allocators, the practical question is not whether the expiry matters — it does — but how to size exposure and hedge between now and the reset. Below we parse the numbers, the likely microstructure mechanics, directional scenarios, and tradeable hedges for both short‑term traders and treasury managers.

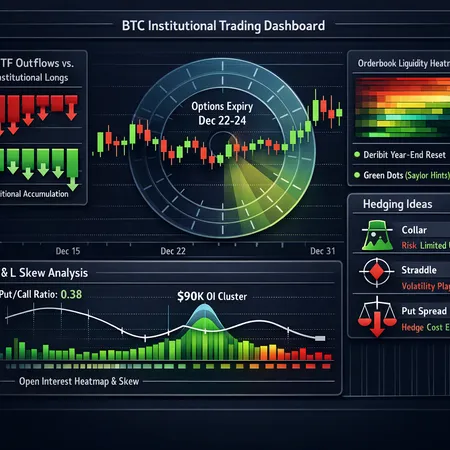

The expiry: size, skew and the meaning of a 0.38 put‑call ratio

Deribit’s year‑end books are unusually large this round — combined bitcoin and ether contracts approach a notional in the tens of billions, with reporting pegging the Bitcoin/Ether aggregate around $27 billion for the Dec. 22–24 expiries. Such scale concentrates gamma and open interest into discrete strikes, increasing the chance of strike‑dependent pinning and short squeezes if spot approaches those levels.source

A reported put‑call ratio (PCR) of ~0.38 for the expiry is materially skewed toward calls — meaning there are far more calls than puts outstanding. Interpreting PCR:

- PCR = puts / calls, so 0.38 implies calls > puts. On the margin, sellers/buyers of calls dominate, signaling a net bullish positioning from options buyers or write-heavy structures from sellers.

- Practically, that can compress upside implied volatility (IV) and expand downside IV if a rapid selloff causes market makers to buy hedges. But because calls are dominant, pinning toward call clusters can occur if delta/gamma exposure hedges need to be wound.

Put the two together: large notional + low PCR = concentrated upside bets that can be amplified by leverage if BTC moves into or through key call strike zones.

ETF flows: nearly $497m in weekly outflows and why spot demand matters

Spot‑Bitcoin ETF flows remain an important barometer of retail and institutional spot demand. Recent data show weekly outflows of about $497 million, a clear signal that marginal spot buying from ETFs has waned during this stretch.source

Why this matters around an options expiry:

- ETFs are a structural buyer of spot; when flows reverse, the natural bid that mops up sell pressure is weaker, creating thinner spot liquidity. That makes squeezes (both short and long) sharper and re‑pricing faster.

- Outflows also reduce natural counterparties for option sellers who delta‑hedge in spot; market makers forced to delta‑hedge through less liquid order books can cause larger moves.

So an expiry biased toward calls meets a market with less spot buy‑support — a recipe for higher realized volatility if exogenous selling pressure arrives.

Margin longs and leverage: the exchange risk layer

Concurrent with the expiry and ETF weakness, exchange data shows margin long positions rising (Bitfinex longs climbed to levels last seen in early 2024), implying retail and speculative bulls are using leverage rather than spot ETFs to express bullish views.source

Why leverage matters:

- Levered positions can be fragile and fuel quick liquidations. A small move against concentrated long exposure can cascade through funding/futures and spot, especially when ETFs are net sellers.

- Combined with a call‑heavy options book, margin longs mean there are two potential upside squeezes (from call gamma and forced deleveraging on upside) or violent downside if the market flips and liquidations cascade.

In short: leverage makes the market more binary around the expiry window.

Institutional signals, liquidity clusters and the $90K neighborhood

Public institutional hints — notably Michael Saylor’s social cues and the so‑called “green dots” — have signaled accumulation and drawn attention to liquidity clusters around $90K as a tactical zone.source

Institutional accumulation tends to be executed off‑exchange (OTC/prime desks) or via large block trades; ETFs are only one channel. The practical implications:

- Large institutional bids near $90K can act as a floor in a panic, reducing realized drawdown if those bids execute.

- However, block buys are episodic — they can provide abrupt support but not continuous liquidity. If on‑exchange liquidity is thin, the execution of those bids can cause quick reversion trades rather than a slow, stable bid.

Combining this with the expiry: liquidity clusters serve as magnets for pinning but can also be the staging ground for violent recoveries if liquidations trigger buys from institutions.

Probabilistic short‑term scenarios (tradeable framings)

Below are three concise scenario frameworks traders can use, with approximate triggers and market mechanics.

Bullish squeeze (probability: medium)

- Trigger: Spot breaks above a large call open interest cluster between current levels and $95K, with funding staying neutral/negative.

- Mechanics: Market makers short calls need to cover, delta hedges create spot buying, margin longs add levered energy, and institutional bids absorb sell‑side gyrations.

- Result: Rapid move higher into expiry days, IV compression on calls but realized vol spikes.

Volatility spike & pin (probability: medium‑high)

- Trigger: Spot drifts into a dense strike band (e.g., $88–92K) with mixed flows; ETFs continue outflows and market makers rebalance gamma.

- Mechanics: Gamma forcing leads to intraday pinning; realized vol rises; short‑dated straddles expensive; risk of transient gaps if liquidity evaporates.

Downside unwind & forced selling (probability: medium)

- Trigger: A sudden macro/ETF‑led block sell or liquidation event pushes spot below the $90K cluster.

- Mechanics: Margin long liquidations cascade, market makers widen IV, puts gain value fast. Institutional bids may step in but only after a repricing.

Each scenario is actionable — the key is sizing, slippage assumptions, and explicit hedging.

Tradeable hedging strategies for traders

Below are practical option and futures tactics sized for active traders looking to monetize or protect around the expiry. Use position sizing and tick risk limits appropriate to your book.

1) Delta‑hedged straddle/strangle (volatility play)

- Rationale: If you expect a volatility spike into expiry without a strong directional bias, buy a near‑ATM straddle or an ATM strangle and delta‑hedge intraday.

- Execution: Buy ATM straddle 7–14 days to expiry; maintain a small delta hedge via futures and rebalance as gamma bites. Watch funding and roll cost.

2) Short‑dated put spread (defined risk downside protection)

- Rationale: Cheaper than buying outright puts; you cap downside cost while retaining some protection.

- Execution: Buy 1x 5–10% OTM put and sell 1x 20–25% OTM put (width depends on horizon). Use this when ETF flows are the main tail risk.

3) Bull risk reversal (directional, cheap protection)

- Rationale: If you’re net bullish but want a hedge, sell a put and buy a higher‑strike call (or buy call/short put). Given the low PCR, calls are priced attractively relative to puts.

- Execution: Buy a slightly OTM call and sell a deeper OTM put, sized to your risk tolerance. Monitor margin requirements — short puts can be capital‑heavy.

4) Gamma scalping for option sellers

- Rationale: If you’ve sold premium into elevated IV, actively gamma scalp as spot moves to improve profitability.

- Execution: Keep tight delta bands and use futures to rebalance; be disciplined about bid/ask and slippage during thin session liquidity.

5) Calendar spreads (play term structure)

- Rationale: Sell short‑dated premium into the expiry and own further‑dated options if you expect term‑structure normalization after expiry.

- Execution: Sell nearest weekly calls/puts centered on likely pin strikes; buy 1–3 month calls/puts as reinsurance.

Hedging frameworks for treasury managers and allocators

Institutional treasuries care about capital preservation, optionality and accounting friendliness. Here are conservative, implementable approaches.

Collars (buy downside protection, cap upside)

- Structure: Buy an OTM put and simultaneously sell an OTM call above where you’re comfortable capping upside.

- Rationale: Collars are cheap (often zero‑cost) and keep upside participation limited but protect large holdings during transient squeezes.

Cash‑secured puts (structured accumulation)

- Structure: Sell PUTs at targeted accumulation price levels, only if you’re comfortable taking delivery or layering cash allocations.

- Rationale: Offers yield while setting a clear buy‑price for allocation programs; pair with size limits to avoid forced purchases during spikes of volatility.

Laddered orders and block OTC execution

- Rationale: To avoid slippage in a thin expiry window, execute block buys through OTC desks or ladder entries in the $85–95K band, especially if institutional bids appear.

- Implementation: Size tranches, pre‑negotiate block fills, and use block auctions to prevent adverse market impact. Bitlet.app clients often balance execution across P2P and OTC rails to reduce market footprint.

Using futures basis and basis hedging

- Rationale: Hedge spot exposure with short futures or swap positions while maintaining directional optionality via options in the spot book.

- Implementation: If futures curve is in contango, weigh basis cost versus the cost of outright options protection.

Execution considerations and risk controls

- Slippage & market impact: Expect elevated spreads and reduced depth around expiry. Model conservative fill assumptions and widen stop/limit bands.

- Margin and cross‑product risk: Short put positions require capital cushions; delta hedges introduce basis and funding‑rate risk.

- Correlation risk: Options on BTC and ETH often move together into major flows — monitor cross‑product exposure.

- Monitoring: Track open interest heatmaps, funding rates and ETF flows intraday. Set automated alerts at key strike bands and liquidity clusters (e.g., $90K).

For many traders, Bitcoin remains the primary bellwether; watching cross‑asset cues and ETF flow updates will be essential during the Dec. 22–24 expiry window.

Practical playbook — checklist for the week

- Identify major open interest clusters and mark them on your DOM.

- Size hedges relative to notional and expected slippage (stress test fills at 2–3x normal spread).

- Keep a portion of dry powder to exploit institutional block bids near $90K.

- Use defined‑risk structures (spreads, collars) if capital restraints matter.

- If selling premium, gamma‑scalp actively and predefine max loss bands.

Final thoughts

This year’s Deribit year‑end reset is not just a calendar event — it is a concentrated liquidity and gamma test. A low PCR (~0.38) and $27bn notional create a bias and a hazard: upside is structurally favored in the options market, but ETF outflows and leveraged margin longs introduce fragility. Institutional bids near $90K add nuance — they can provide support, but they are not a substitute for continuous market depth.

Active traders should approach with scenario‑based sizing and explicit delta/gamma plans. Treasuries should prefer defined‑risk hedges (collars, cash‑secured puts, block OTC execution) to preserve capital while maintaining optionality. Monitor flows, funding, and open interest heatmaps, and remember that in thin markets, microstructure matters as much as macro views.

Sources

- Coindesk: Boxing‑day bonanza — USD27 billion in Bitcoin, Ether options set for year‑end reset

- Crypto.NEWS: Bitcoin price stalls at 89K as weekly ETF outflows top nearly $500m

- Coindesk: Bullish Bitcoin plays on Bitfinex swell to highest since early 2024

- TheNewsCrypto: Saylor hints at Bitcoin buy as BTC tests 90K resistance zone