Oracle Failures in DeFi: Deep Dive on the Moonwell cbETH Mispricing and Hardening Steps

Summary

Executive summary

On the morning of the incident, Moonwell’s cbETH market was fed a mispriced oracle value that pegged cbETH near $1, a dramatic disconnect from its expected market value. The error cascaded into roughly $1.78M of bad debt for Moonwell as borrowing and collateral calculations used the corrupted price feed. This article reconstructs the timeline and mechanics of the mispricing, explains why liquid staking tokens (LSTs) such as CBETH are particularly fragile to oracle errors, examines how automated/AI-coded oracle logic can introduce new failure modes, and translates those lessons into concrete mitigations and a post‑mortem checklist for lenders and auditors.

Read this if you are a DeFi engineer, protocol risk lead, or auditor responsible for hardening markets against oracle risk, particularly for LST markets like CBETH (Moonwell uses the WELL token in governance and protocol economics).

What happened: timeline and mechanics of the cbETH mispricing

Early: cbETH price oracle began publishing values far below market consensus; at one point it was priced near $1. The mispriced feed was used by Moonwell’s lending markets to value collateral and calculate borrows. For a thorough incident writeup see this report on the mispricing and resulting bad debt. (Immediate source: Moonwell oracle mispricing and drain).

Propagation: Smart contracts that trust the oracle updated internal accounting. Borrow positions were allowed to remain open against overvalued collateral or underpriced assets depending on the direction of the error, producing bad debt when positions could not be liquidated cleanly.

Resolution: The team had to reconcile on‑chain accounting, inject reserves/coverage, and adjust risk parameters across markets to stem further losses. The incident shows a classic pattern: a single corrupted data input — an oracle quote — propagates through composable financial primitives and creates systemic exposure.

Why $1.78M matters: beyond the headline number, this figure represents both immediate protocol capital shortfall and a demonstrable governance and operational gap in the oracle‑to‑risk pipeline. A relatively modest misprice becomes protocol‑scale when leverage, collateral factors, and liquidation mechanics are tuned without adequate fallbacks.

Why liquid staking tokens (LSTs) like cbETH are uniquely exposed

Liquid staking tokens are not simple token‑for‑token price pegs. cbETH represents staked ETH plus accrued rewards and therefore tracks an exchange rate (ETH per cbETH) that drifts slowly as rewards accumulate. Two structural features make LSTs different:

Dual dependence: the token price depends on both ETH’s spot price and the protocol exchange rate (cbETH ↔ ETH). Mispricing of either leg — the exchange rate or ETH price — can produce large valuation errors.

Lower liquidity and fragmented markets: some LSTs trade on fewer venues than ETH; a corrupted or thinly sourced oracle can stray far from aggregated market pricing.

Staking concentration and product structure: with staking services and ETFs concentrating staking flows (e.g., large custodians offering liquid staking exposure), the effective price dynamics of LSTs can change rapidly during redemptions, withdrawals or ETF staking flows. See discussion of staking concentration in relation to liquid staking tokens and ETFs for policymakers and risk teams in this analysis on ETF staking dynamics. (Context: BlackRock’s Ethereum ETF and aggressive staking).

Because cbETH’s value is a function of ETH price × exchange rate, an oracle that fails to combine both data points correctly — or that ingests a corrupted exchange rate — can report a grossly inaccurate USD value. In Moonwell’s case the feed produced a price that did not reflect the on‑market cbETH value, creating margin and liquidation failures when automated accounting used that price.

How automated and AI‑assisted oracle systems can fail

Automation and AI are often introduced to reduce latency and human toil, but they add subtle failure modes:

Parsing and transformation errors: automated agents that convert on‑chain or off‑chain attestations into numeric quotes can misparse symbols, decimal places, or unit conversions (for LSTs this could be misapplying the exchange rate multiplier).

Model brittleness: AI models trained on historical patterns may produce nonsensical outputs when confronted with novel market regimes or partial data, e.g., during extreme ETF flows or post‑merge withdrawal dynamics.

Aggregation blindspots: naive aggregators that simply average or take the latest feed without outlier rejection can be manipulated or corrupted by a single misbehaving source.

Latency vs freshness tradeoffs: TWAPs reduce spoofing risk but can lag during fast markets; aggressive single‑tick feeds reduce staleness but increase susceptibility to manipulation.

Dependency chains and human oversight gaps: automated oracles often rely on multiple third‑party services (relayers, indexers, data vendors). An error in any link can cascade, and teams can be blind to it until it's too late.

The incident writeup notes an AI‑coded oracle glitch — a reminder that adding machine logic to the stack requires the same discipline we apply to smart contracts: tests, audits, failover plans and explicit on‑call procedures. Market stress can magnify failure probability; for example, ETF outflows and technical headwinds in the ETH market increase the chance of data anomalies that confuse models (see market context about recent ETF outflows and technical signals). (Market context: Ethereum ETF outflows extend into fourth month).

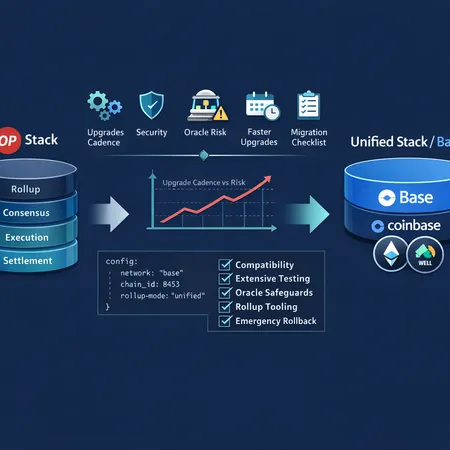

Practical mitigation strategies — design patterns and operational controls

Below are practical recommendations organized by category. These are prescriptive but should be adapted to your protocol’s risk tolerance, capital buffers, and user base.

Oracle design and engineering

Multi‑source aggregation with robust statistics: ingest at least three independent feeds and compute a median of medians or clipped mean. For LSTs ensure the aggregator combines (1) ETH spot price sources and (2) exchange‑rate sources correctly, and cross‑validates the two legs.

Unit and decimal safety: canonicalize decimals and units before any arithmetic and include contract‑level asserts for plausible ranges (e.g., reject cbETH exchange rates that imply >30% intraday yield).

TWAP + spot hybrid: use a hybrid where your oracle publishes both a short TWAP (e.g., 5–15 minutes) and the last trade price; smart contracts use the TWAP by default but accept spot for liquidations under stricter safety checks.

Oracle signing and provenance: track which data providers contributed to each published observation, store provenance on chain for post‑incident forensics, and require multiple signatures for high‑impact markets.

Fallback pricing & circuit breakers

Fallback oracles: maintain an on‑chain fallback that uses a different aggregation method or a lower‑frequency anchor (e.g., a 1‑hour TWAP) if the primary feed deviates beyond a tolerance.

Circuit breakers and sanity checks: reject price updates that exceed a configurable percentage change within a timeframe (e.g., >15% move in 5 minutes for cbETH relative to ETH). Trigger a ‘soft pause’ or switch markets to restricted mode where borrows cannot increase.

Emergency pause with governance and multisig: have an on‑chain governor or guardian that can pause new borrows/withdrawals for affected markets while allowing withdrawals for healthy positions where feasible.

Risk parameter tuning (protocol-level)

Conservative collateral factors for LSTs: start with lower collateral factors and smaller debt ceilings for newly supported LST markets; consider dynamic collateral factors that tighten as the exchange rate volatility or market stress rises.

Leverage and liquidation design: widen liquidation incentives and tighten thresholds for LSTs under stress. Ensure liquidation auctions do not rely on the same price feed without extra validation.

Reserve buffers and supply caps: maintain a protocol reserve fund sufficient to cover tail‑risk exposures and set supply or borrow caps per asset to limit single‑asset concentration (especially for LSTs tied to large custodians or ETFs).

Comptroller & insurance settings

Auto‑managed insurance pools: allocate a percentage of interest revenue into an insurance pool sized for a worst‑case scenario tied to observed oracle failure histories.

Granular market controls: provide the comptroller with per‑market switches to tune collateral factors, borrow caps, and liquidation incentives quickly and on‑chain.

Reorg and stale oracle handling: detect long reorgs and do not accept oracle updates that predate a recent deep reorg without revalidation; ensure the comptroller references block timestamps and block numbers when making time‑sensitive valuation decisions.

Monitoring, alerting, and chaos testing

End‑to‑end monitoring: instrument the entire price pipeline with SLA metrics, latency histograms, and divergence alerts between primary and fallback feeds.

On‑call runbooks and drills: create an incident runbook that covers common failure modes: mispriced exchange rates, single source drift, aggregator poisoning, and reorgs. Runtabletop and live drills quarterly.

Chaos testing and adversarial simulations: simulate oracle poisoning, stale feeds, feed pauses, and large directional moves using a testnet environment to validate failovers and governance responses.

A compact post‑mortem checklist for DeFi lenders and risk teams

This checklist is intended to be operational and audit‑ready. Use it immediately after an oracle incident and keep it as part of your incident response toolkit.

Triage & isolate

- Freeze new borrows/market interactions for affected markets if there is unexplained price divergence.

- If possible, prevent protocol state changes that depend on the suspect feed.

Confirm provenance & timeline

- Export oracle logs and provenance (signers, timestamps, source endpoints).

- Map exactly which transactions used the corrupted price and capture affected block ranges.

Quantify exposure

- Compute gas‑costed replays of affected liquidations, accounts rendered undercollateralized, and resulting bad debt.

- Produce a minimal set of account snapshots for governance and accounting.

Short‑term containment

- Flip affected markets to fallback TWAP or pause them entirely.

- Deploy compensating parameter changes in the comptroller (lower collateral factors, increase liquidation thresholds) to prevent additional debt buildup.

Capital remediation

- Cover immediate bad debt using the insurance pool or emergency multisig transfer.

- Consider a temporary governance proposal for replenishment (optionally via treasury or revenue diversion).

Root cause analysis

- Was the error data (exchange rate, ETH price) incorrect? Was the aggregator logic wrong? Was a model producing nonsensical output?

- Identify whether this was a data issue, logic error, or an attacker exploiting a known gap.

Remediation & tests

- Patch the oracle code and add unit/integration tests reproducing the failure.

- Add new monitors for the exact failure mode and run regression tests.

Communication & audit

- Publish a transparent incident report with timelines, affected PVs, and remediation steps.

- Engage an external audit or third‑party oracle specialist for a 72‑hour review where appropriate.

Governance lessons

- Update governance playbooks: voting thresholds for emergency actions, time delays, and multisig policies.

- Reassess which assets are enabled by default and require special approval (especially LSTs).

Key takeaways for protocol architects and auditors

Oracle failures are not hypothetical: they create economic loss quickly. The Moonwell cbETH mispricing and its ~$1.78M bad debt illustrate how a single corrupted input can create outsized protocol risk (incident report).

LSTs like cbETH have compound exposure (ETH price × exchange rate). Treat them as a special class of collateral with conservative caps, independent feed cross‑checks, and tighter liquidation mechanics.

Automation and AI reduce friction but introduce new failure modes. Instrument models, require provenance, and keep human‑in‑the‑loop emergency controls for critical markets.

Design for graceful failure: fallback oracles, circuit breakers, reserves and per‑market caps are all first‑order defenses.

Post‑incident discipline matters: forensics, transparent reports, and follow‑through on remediation and testing will materially reduce recurrence risk.

For teams building and operating lending markets — whether at a standalone protocol or a service like Bitlet.app that integrates multiple on‑chain services — these are concrete, operational steps you can begin implementing today.

Sources

- Moonwell cbETH mispricing and bad debt report: https://crypto.news/moonwells-ai-coded-oracle-glitch-misprices-cbeth-at-1-drains-1-78m/

- Analysis of staking concentration and liquid staking token dynamics: https://cryptoslate.com/blackrocks-ethereum-etf-aims-for-aggressive-staking/

- Ethereum market context and ETF outflows: https://crypto.news/ethereum-price-forms-death-cross-as-etf-outflows-extend-into-fourth-month-will-it-crash/

For further reading on how oracle design choices affect liquidation dynamics, see research pieces and protocol post‑mortems across the ecosystem — and consider adding chaos tests to your CI pipeline as a low‑cost, high‑impact control.

(Internal references: for broader market context on how oracle risk affects other asset classes, check DeFi commentary and the historical price signalling role of Bitcoin.)