Market Structure Headwinds: Binance Delistings, Slowing USDT Demand and Liquidity Risk

Summary

Executive snapshot

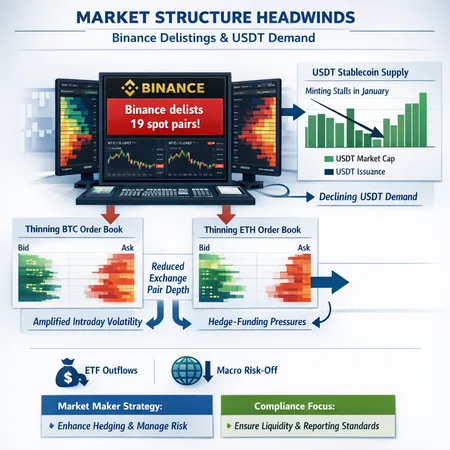

Recent exchange-level moves and macro flow shifts are reshaping short-term crypto market structure. Binance announced a programmatic delisting of 19 spot trading pairs — affecting categories from DeFi and memecoins to pairs denominated against major bases — while market data shows USDT demand and stablecoin minting stalled in January. Add to that approximately $1B of ETF outflows tied to macro volatility, and you have a confluence that reduces on-exchange pair depth, increases spread and market-impact, and elevates execution risk for institutional participants.

This post dissects why exchanges prune pairs, what the data on USDT demand implies for intraday funding and hedge flows, how ETF outflows amplify the problem, and practical hedging and liquidity strategies for traders and market makers.

Why exchanges prune spot pairs (what Binance did and why)

Exchanges regularly remove low-utility pairs to concentrate liquidity, lower operational complexity, and reduce risk exposure. Binance’s announcement to delist 19 spot pairs is a prime example: the move targeted a mix of low-turnover DeFi and meme tokens and pairs quoted against major bases, trimming the long tail of thinly traded markets (Binance delistings announcement).

Why this matters: when an exchange removes a pair it effectively collapses that local order-book. Even if liquidity exists in the underlying token elsewhere, the immediate effect is less depth on the platform where many algos and hedges execute. For market makers, fewer pairs mean: tighter capital concentration on remaining markets, potential increase in inventory imbalance risk, and higher sensitivity to single-venue shocks.

Typical motivations behind pruning:

- Low volume and poor quoted spread quality that drag liquidity provider returns.

- Regulatory or compliance concerns tied to specific tokens or jurisdictions.

- Operational simplification (fewer markets to monitor, cold-wallets, risk rules).

- Product rationalization: focusing liquidity on high-demand base pairs like BTC and ETH.

For many desks, Bitcoin and Ethereum-denominated markets act as primary rails for cross-asset hedges. Removing peripheral pairs forces more execution through those bases, which can concentrate order flow and compress or skew depth in unexpected ways.

The stablecoin plumbing: USDT demand stalling and why it matters

Stablecoins, especially USDT, are the plumbing that fuels intraday funding, margin transfers and cross-venue arbitrage. Recent data indicates USDT minting and demand stalled in January, a signal that funding liquidity growth has slowed and that stablecoin-driven transaction volume may be softer than it was in prior months (USDT demand stalls in January).

Practical implications:

- Fewer newly minted USDT means smaller incremental inventory for market makers and arbitrageurs to deploy as collateral for opening positions or bridging between venues.

- Slower stablecoin inflows reduce the amplitude of arbitrage legs that normally keep spot, futures and perpetual markets aligned intraday; funding-rate arbitrage and basis trades become harder to scale.

- Counterparties that relied on easy access to freshly minted USDT may lengthen settlement times or move to other stablecoins (USDC, BUSD), fragmenting liquidity between rails.

The net effect is less nimble intraday funding and a higher execution tax for spreads and market-impact.

ETF outflows and macro volatility: the external squeeze

Institutional flows compound the picture. Recent reporting showed around $1B of net outflows from Bitcoin and Ether ETFs as macro volatility pushed institutions to reduce risk exposure (ETF outflows and macro volatility). When allocators redeem ETF exposure, the resulting selling pressure and settlement demands can drain liquidity from on-exchange books and reduce market-making appetite.

How these pieces interact:

- ETF outflows remove long-duration liquidity: large sellers dump into the spot or use derivatives to hedge, increasing short-term supply pressure.

- Combined with stalled USDT demand, the natural buyers that absorb these flows (arbitrage desks, stablecoin-funded market makers) are smaller or slower, so price dislocations endure longer.

- Exchange delistings make specific venues less attractive for absorbing flows, pushing trades to fewer order-books and elevating market impact.

This triad — delistings, stablecoin slowdown, and institutional outflows — creates a market environment where volatility can spike on relatively modest triggers.

How reduced pair depth amplifies volatility (mechanics)

Reduced pair depth increases price sensitivity to executed size. A thin order book means a market order consumes multiple price levels, generating a larger immediate swing. Key mechanics:

- Market-impact scales with depth: a standard linear or square-root impact model implies slippage increases faster than order size when depth is low.

- Wider spreads: market makers widen quotes to compensate for inventory and adverse selection risk, raising execution costs for takers.

- Cross-venue contagion: when liquidity pools fragment, an aggressive move on one venue cascades as algos reprice on linked markets.

- Funding and basis instability: with weaker arbitrage flows (stalled USDT minting), divergences between spot, futures and perpetual markets persist, causing funding-rate shocks.

For professional desks this means higher realized volatility, larger tail risk, and greater difficulty executing large blocks without notifying counterparties or using OTC channels.

Practical hedging and liquidity strategies for traders and market makers

Adaptation is practical and operational. Below are actionable strategies organized by role.

For professional traders:

- Pre-trade liquidity checks: always snapshot top-of-book depth and 5–10 levels of the order book; compute estimated market-impact before sending a taker order.

- Use algorithmic execution (TWAP/VWAP/POV) with adaptive participation limits and dynamic spread-aware slicing.

- Favor limit orders where possible; if a taker hit is required, split across venues or use mid-point peg orders to reduce spread cost.

- Maintain multi-stablecoin balances (USDT, USDC, BUSD) to avoid single-rail funding bottlenecks.

- Consider using options collars or protective stops sized to expected slippage, not just nominal stop distances.

For market makers:

- Recalibrate quoting widths and size by venue: concentrate risk capital on deeper venues but keep a presence on trimmed pairs to capture occasional alpha.

- Increase monitoring of filling-to-quoted ratios and inventory skew; dynamically adjust hedge ratios with futures or options rather than relying solely on spot crosses.

- Use cross-exchange hedging: hedge inventory on a deep external venue if your local pair was delisted or thinned.

- Manage funding liquidity proactively: secure committed lines, maintain stablecoin reserves, or arrange prime-broker liquidity to avoid being forced into adverse unwinds.

For both roles, leverage OTC and block trading when moving large sizes to avoid signaling and order-book churn. Platforms and hybrid solutions — including P2P and OTC liquidity providers — become more valuable when on-exchange pair depth is low.

Execution architecture and routing

- Smart order routers should be tuned to include depth-weighted costs, not just best price.

- Implement latency-aware routing: cheaper-looking prices on a distant venue are not free if cancellations or partial fills force manual intervention.

- Use midpoint-peg and post-only strategies aggressively during thin markets to control price impact.

Compliance and operational controls for officers

Compliance and risk teams must broaden their surveillance and stress tests:

- Monitor exchange announcements and delisting schedules as part of liquidity risk indicators; establish pre-approved migration paths for affected products.

- Update approval thresholds for API order sizes and automated strategies when venue depth drops below pre-set bands.

- Audit counterparty and on-chain settlement exposure to alternative stablecoins if USDT issuance stalls, ensuring AML/KYC coverage for new rails.

- Run scenario analyses that combine delisting, stablecoin shortage, and ETF redemption shocks to quantify liquidity shortfalls and client margin implications.

Quick playbook checklist

- Snapshot exchange depth and projected market-impact before each large trade.

- Maintain multi-rail stablecoin balances and confirmed OTC relationships.

- Use algorithmic slicing with venue-aware parameters, or route blocks to dark/OTC liquidity.

- Reprice market-making algorithms to account for wider expected spreads and inventory risks.

- Stress-test systems against combined delisting + stablecoin slowdown + ETF outflow scenarios.

Final thoughts

Exchange-level pruning like Binance delistings, slowing USDT demand and ETF outflows are not isolated events — they interact to reduce on-exchange pair depth and raise the cost of execution. Market participants who treat liquidity as a dynamic, cross-venue problem will navigate the current headwinds better than those who rely on static assumptions about spreads and execution risk. Keep an eye on stablecoin issuance, monitor ETF flow reports, and adjust hedging frameworks accordingly — and remember that tools ranging from smart routers to OTC desks and alternative stablecoins can materially reduce tail exposure.

Platforms that centralize cross-venue order routing and settlement details—Bitlet.app among them—can help traders maintain visibility and access to liquidity rails during these transitions.

Sources

- Binance delistings announcement: https://u.today/binance-announces-major-19-pair-delisting-with-defi-ai-meme-coins-bitcoin-and-ethereum-in-focus?utm_source=snapi

- USDT demand stalls in January: https://beincrypto.com/usdt-demand-stalls-in-january/

- Bitcoin & Ether ETF outflows and macro volatility: https://invezz.com/news/2026/01/22/bitcoin-ether-etfs-see-around-1b-in-outflows-as-macro-volatility-spurs-risk-reduction/?utm_source=snapi