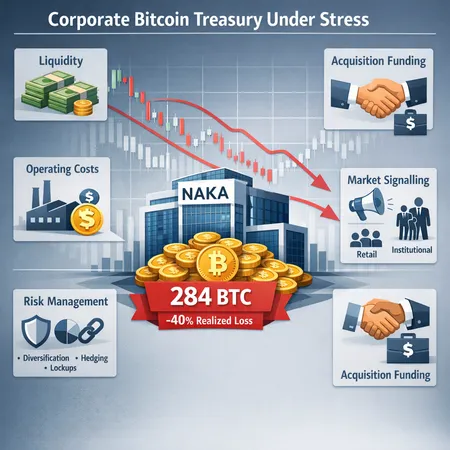

When Corporate Bitcoin Treasuries Crack: Lessons from Nakamoto Inc.'s 284 BTC Sale

Summary

Executive summary

Nakamoto Inc.'s decision to sell 284 BTC in March — reportedly at a substantial loss — exposed how fragile the "corporate bitcoin treasury" narrative can be when a listed firm faces operational or liquidity strain. The sale, documented in company filings and covered by multiple outlets, crystallized a few inconvenient truths: public treasuries can become forced liquidity sources, realized losses have outsized signaling effects, and equity markets punish both the hit and the perceived governance lapse.

For many traders, Bitcoin remains the primary market bellwether, so moves by public treasuries are more than accounting footnotes. This piece lays out the facts of the Nakamoto sale, explores motives behind corporate crypto sales, examines market and equity reactions (including the NAKA share drop), surveys precedent among listed treasury firms, and proposes pragmatic risk-management frameworks for treasurers and analysts.

The facts: what Nakamoto did and what the filings show

In late March, filings and market reports revealed that Nakamoto Inc. offloaded 284 BTC — roughly 5% of its disclosed holdings — to shore up operations as part of a broader restructuring. Coverage from Coindesk notes the sale represented an operational liquidity move, while Bitcoin.com and Crypto.News highlight the sale occurred below cost basis and materially reduced other exposure (including a reduced stake in Metaplanet). Blockonomi reported an immediate equity reaction: NAKA shares fell roughly 7% after the news.

- Coindesk: reported the company offloaded roughly 5% of its bitcoin holdings in a liquidity context (Coindesk coverage).

- Bitcoin.com: filed reports detail the sale below cost basis to fund operations (Bitcoin.com article).

- Crypto.News: additional reporting on the reduction of crypto exposure amid restructuring (Crypto.News article).

- Blockonomi: covered the equity market reaction — NAKA shares tumbled after the fire sale (Blockonomi article).

Company documents suggest the sale realized an approximate ~40% loss relative to Nakamoto’s cost basis on those coins. That loss was recognized on the income statement, creating a direct hit to reported earnings and shareholders’ equity.

Why public treasury firms sell: liquidity, costs, and strategic funding

There are three pragmatic reasons a firm with a public bitcoin treasury might sell:

- Liquidity for operations: public companies face payroll, vendor bills, interest costs, and other cash needs. In stress scenarios, digital assets are a fast source of liquidity.

- Funding strategic moves or acquisitions: crypto holdings can be tapped to finance M&A or capital allocation when cash is constrained.

- Debt or covenant management: margin calls, loan covenants, or refinancing needs can force sales.

All three drivers are prosaic — they’re the same reasons firms sell any liquid asset. The difference with Bitcoin is optics and price volatility: a sale can crystallize a headline loss and act as a negative signal to markets about a firm’s health.

Market signaling: why a corporate sale magnifies price and confidence effects

When a listed firm sells a material crypto position, it sends two signals simultaneously:

- Financial signal: the company needed cash — that can be read as a sign of operational weakness or deteriorating balance-sheet health.

- Informational signal: insiders may be changing beliefs about future price trajectory, prompting investors to re-evaluate valuation.

Retail investors often overreact to narratives — a sale framed as a "fire sale" amplifies fear and can pressure price further, while algorithmic and quant funds respond to both realized volume and news flow. Institutional holders watch the signal too; repeated corporate selling can lower confidence in the idea that public treasuries are durable macro buyers.

The Nakamoto episode demonstrates this loudly: the sale was both a realized loss and a visible signal that a public treasury can be tapped in stress — a combination that hurt NAKA’s equity value almost immediately.

Valuation and equity reaction: reading the NAKA move

NAKA shares dropped after the sale announcement — a predictable reaction given the magnitude of the realized loss and the perceived question marks around governance and liquidity planning. Equity investors price both the immediate earnings hit and the higher probability of future dilution or cash raises.

Two valuation channels are worth separating:

- Direct P&L channel: realized losses reduce earnings and book equity; for firms trading on thin multiples, that alone can drive shares lower.

- Confidence/flow channel: visible selling can change investor expectations of future treasury behavior, increasing required risk premium or lowering future growth estimates.

Blockonomi's coverage of a ~7% tumble in NAKA is evidence of both channels in action. For equity analysts, it's a reminder to stress-test models for scenarios where treasury holdings are partially liquidated and to incorporate disclosure on sale triggers and governance.

Precedent and context: not all listed holders behave the same

There is meaningful variance across firms that report bitcoin treasuries. Some, like MicroStrategy, have historically prioritized accumulation and have structured messaging and financing around that strategy. Others — particularly smaller or less diversified listed firms — have at times sold to fund operations or de-risk positions.

The Nakamoto case sits closer to prior episodes where companies with thinner cash reserves or operational stress sold crypto to meet obligations. The lesson: headline-grabbing accumulation policies need matching liquidity and covenant plans, otherwise the company risks being a forced seller when markets are weakest.

Risk management frameworks for public crypto treasuries

Treasurers and boards should treat crypto holdings like any strategic asset class: they require formal policies, governance, and stress testing. Recommended components:

Treasury policy and governance

- Formal treasury mandate: written objectives for why crypto is held (store-of-value, strategic exposure, liquidity reserve), thresholds for what fraction of balance sheet may be in crypto, and authorized sale triggers.

- Board oversight: regular reporting, independent audit of holdings, and scenario reviews.

Diversification and liquidity layering

- Staggered holdings: maintain a mix of liquid fiat, stablecoins, and crypto to avoid a single point of failure.

- Liquidity ladder: identify how much can be monetized in minutes, days, and weeks under different market conditions.

Hedging and derivatives

- Use futures and options to hedge downside risk without crystallizing losses immediately; collars and put overlays can limit realized damage while preserving upside exposure.

- Consider cash-secured hedges or OTC trades with reputable counterparties to manage execution risk.

Lockups, commitments, and disclosure

- Lockups or multi-year commitments from founders/insiders reduce fear of dumping and align incentives.

- Transparent, standardized disclosure (timing, counterparties, realized/unrealized P&L) reduces information asymmetry and calms markets.

Stress-testing and contingency planning

- Run reverse-stress tests: what market moves + corporate events would force sales? Define playbooks for staged monetization rather than fire sales.

- Maintain covenant buffers and committed credit lines that are not contingent on crypto valuations.

What this implies for the 'corporate treasury as macro buyer' narrative

The popular narrative that publicly listed bitcoin treasuries act as consistent macro buyers is over-simplified. In calm markets, many treasuries may accumulate. Under stress, however, the same treasuries can flip to sellers to meet operations, service debt, or fund restructuring.

Nakamoto's sale is a salutary case: it underscores that corporate treasuries are only as robust as their governance, liquidity planning, and access to non-crypto buffers. For the market, the implication is that corporate accumulation should be treated as conditional — not a guaranteed bid under every macro scenario.

Practical checklist for investors, analysts, and treasurers

- Demand and publish a formal treasury policy with explicit sale triggers.

- Stress-test balance sheets for scenarios that would force monetization.

- Insist on diversified liquidity (cash + stable yield options) to avoid knee-jerk selling.

- Explore hedging strategies (options/futures) to protect downside without killing upside exposure.

- Monitor insiders’ and executives’ behaviors and lockup arrangements; transparency matters.

Analysts should add a treasury-discount scenario into valuations and model what partial monetization does to EPS, cash runway, and shareholder dilution.

Conclusion

Nakamoto Inc.'s 284 BTC sale — and the roughly 40% realized loss reported — is more than a single-company story. It's a reminder that corporate bitcoin treasuries introduce both opportunity and risk. Without rigorous policy, diversified liquidity, and hedging, public holders risk turning a strategic asset into a forced liability under stress.

For corporate treasurers and investors evaluating BTC allocations, the message is practical: design for the stress case, disclose clearly, and avoid depending on the myth that corporate treasuries are always the market's backstop. Platforms like Bitlet.app make it easier for firms to explore diversified crypto liquidity options, but the real resilience comes from governance, contingency planning, and sober disclosure.

Sources

- https://crypto.news/nakamoto-sells-284-btc-reduces-metaplanet-stake-amid-restructuring-push/

- https://news.bitcoin.com/david-baileys-nasdaq-listed-bitcoin-firm-nakamoto-sells-284-btc-below-cost-basis/

- https://www.coindesk.com/markets/2026/03/31/david-bailey-s-nakamoto-sells-roughly-5-of-its-bitcoin-holdings-offloading-284-btc

- https://blockonomi.com/nakamoto-naka-shares-tumble-7-following-bitcoin-fire-sale-at-steep-discount/