What ECB Acceptance of Tokenized Securities Means — and Why the XRP Ledger Is ‘In the Mix’

Summary

Executive snapshot

The European Central Bank’s reported openness to accepting tokenized securities as eligible collateral marks a practical pivot: not just academic talk about digital assets, but a pathway to on‑chain settlement touching central bank balance sheets. That doesn’t instantly replace existing plumbing — it changes the shape of liquidity, settlement windows and custody requirements for both commercial banks and central banks. The fact that the XRP Ledger is explicitly “in the mix” matters because it offers a set of performance and cost characteristics that align with institutional needs: high throughput, low fees and predictable settlement finality.

What “tokenized collateral” actually means for central and commercial banks

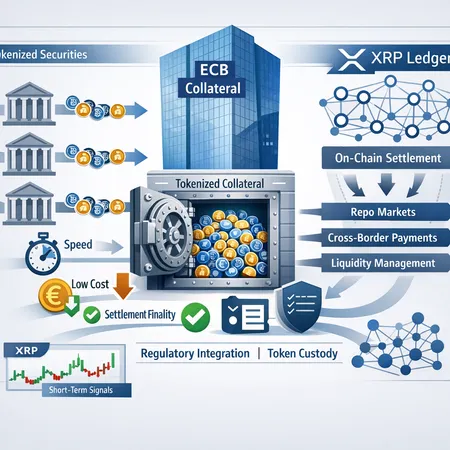

Tokenized collateral refers to traditional asset claims — bonds, repo positions, short‑term paper — represented as cryptographic tokens on a distributed ledger. When the ECB says it will consider tokenized securities as collateral, it is signalling that it will treat some digital representations of securities as equivalent to conventional collateral for operations such as standing facilities or credit operations.

On the operational side this implies at least three concrete changes. First, the mechanics of collateral transfer can move from message‑based post‑trade processes to atomic on‑chain transfers, shortening the time between trade and usable collateral. Second, collateral mobility improves: tokens can be re‑pledged or rehypothecated programmatically and near‑instantly, increasing effective market liquidity. Third, settlement windows and intraday liquidity management change: central banks and treasuries will need to reconcile token positions with ledger states in real time rather than with batch reconciliations at day‑end.

For commercial banks, those changes are not just technical. Accepting tokenized collateral as usable central bank collateral affects capital planning, liquidity coverage ratios and contingency funding frameworks. Banks will need systems that can 1) originate tokenized instruments in a compliant way, 2) move them on‑chain when necessary for repo or intraday operations, and 3) demonstrate to supervisors that on‑chain transfers are legally enforceable and operationally resilient.

Why the ECB moving here matters for market structure and regulatory integration

Regulatory acceptance is the gating factor for institutional adoption. If the ECB validates tokenized collateral, market participants gain a clear template for how on‑chain assets interact with central bank money and monetary policy tools. That reduces legal and operational uncertainty and accelerates the formation of custody markets, settlement relays and integration layers between legacy payment systems and distributed ledgers.

This is regulatory integration in practice: rules and operational standards that allow off‑chain regulated entities to use on‑chain instruments without creating regulatory arbitrage. The ECB’s posture influences national competent authorities, central securities depositories and large custodians to build compatible interfaces rather than insisting on bespoke solutions. For institutions evaluating infrastructure, this moves tokenization from a fringe innovation toward mainstream financial plumbing.

Why the XRP Ledger being “in the mix” is significant

Not all distributed ledgers are created equal for institutional settlement. The XRP Ledger (XRPL) brings three practical attributes often prioritized by treasury desks:

- Speed: XRPL settles transactions in ~3–5 seconds under typical conditions, enabling rapid collateral movement and minimizing intraday exposure windows. Faster settlement shrinks settlement risk in repo and short‑term funding markets.

- Low cost: Transaction fees on XRPL are tiny compared with many smart‑contract platforms. For high‑frequency collateral operations, micro‑fees reduce operational friction and make regular rebalancing cost‑efficient.

- Deterministic settlement finality: XRPL uses a consensus algorithm that yields clear, deterministic finality for transactions, which helps legal departments argue that an on‑chain transfer is completed and irrevocable — a key requirement for central bank collateral operations.

These are precisely the performance characteristics that central bank operations and high‑volume repo desks value. They are also why press reports list XRPL among ledgers under consideration for ECB‑related tokenization pilots: the ledger’s mix of throughput, cost and settlement model fits the plumbing requirements for collateralized liquidity operations rather than speculative DeFi experimentation. For context on the ECB’s position, see the reporting that links tokenized securities and the XRP Ledger as options under evaluation.

Practical use‑cases where tokenized collateral + XRPL could change the game

Below are concrete use‑cases where tokenized collateral integrated with a ledger like XRPL can deliver value:

Repo and secured funding markets

Repos are fundamentally collateralized short‑term loans. Tokenized securities that are accepted by the ECB as collateral could be moved on‑chain and pledged programmatically in moments, enabling near‑real‑time access to central bank liquidity and reducing settlement windows that currently require telephone instructions, batch messaging and reconciliation.

Cross‑border liquidity and intraday central bank access

Tokenized assets combined with a fast settlement ledger enable regional banks to shift collateral across borders quickly, alleviating FX and local regulatory frictions. That’s especially meaningful in tight markets where intraday liquidity matters. On‑chain settlement can be an efficient on‑ramp to central bank facilities when those facilities accept tokenized collateral.

Liquidity management and rehypothecation automation

Programmatic rules can automate re‑pledging and substitution of collateral conditioned on credit limits or triggers, improving collateral efficiency across a bank’s balance sheet. This automation reduces manual operational strain and allows treasuries to run leaner collateral buffers while maintaining safety.

Cross‑platform settlement rails for institutional flows

A ledger with low fees and fast finality can act as a settlement hub that connects custodians, trading venues, and central counterparties (CCPs). That lowers settlement latency and enables richer composability between tokenized instruments and payment systems.

Short‑term market signals for XRP: network usage and price expectations

The market is already reacting to the narrative that tokenized securities and ledger inclusion could drive demand for XRP and XRPL‑based flows. Network metrics reported recently show a jump in activity: one report notes on‑chain activity tripled to roughly 3 million operations, a signal that more participants are interacting with the ledger and potentially testing use‑cases or trading activity. This kind of network momentum matters because adoption often follows consistent operational usage rather than headlines alone.

On the price front, market commentary and prediction markets have priced ahead expectations: some short‑term price models and market sentiment pieces indicate bullish targets for XRP in the near term as adoption narratives mount. That said, institutional engagement will depend more on legal certainty and custody than on short‑term price moves; commercial balance‑sheet decisions are rarely driven by volatile retail speculation. For recent reporting on network activity and market pricing context, see the analyses that document both the surge in on‑chain activity and the market positioning for March 2026.

Custody, compliance and operational changes banks must implement

For banks to use tokenized securities as collateral — and to move them on ledgers such as XRPL — several concrete custody and compliance upgrades are needed:

- Regulated token custody: Banks will require custody solutions that are licensed, auditable and that support features like multi‑party control (MPC signatures), secure key management, and proof of possession without exposing private keys. Custody providers must be integrated into banks’ risk and audit frameworks.

- Legal wrappers and enforceability: Tokenized instruments must have legal status equivalent to their paper or book‑entry counterparts. This often requires standardized legal agreements, clear documentation of title transfer mechanics on‑chain, and alignment with national insolvency and property law.

- KYC/AML and transaction monitoring: On‑chain flows must be reconciled with off‑chain KYC/AML processes. Banks will need tooling to monitor token flows, link on‑chain addresses to legal entities, and generate audit trails acceptable to supervisors.

- Interoperability and messaging bridges: Banks will need secure, reliable bridges between core banking ledgers, custody systems and the token ledger. These bridges must preserve atomicity for collateral transfers (i.e., avoid situations where cash moves without collateral or vice versa).

- Operational resilience and recovery plans: Institutions and the central bank must agree on incident response, dispute resolution and ledger outage procedures. Operational playbooks that account for cross‑ledger recovery are essential.

These changes are substantial but tractable. Large custodians, technology providers and clearing houses are already prototyping standards; what the ECB’s stance does is provide the incentive for those prototypes to harden into production workflows.

Practical risks and outstanding questions

Even with promise, several open questions remain before widescale adoption:

- Legal finality vs. central bank money: Will tokenized collateral settled on an external ledger be considered the same as collateral held on a central bank ledger? The answer affects liquidity ratios and loss‑absorption calculations.

- Interoperability and fragmentation: Multiple ledgers vying to be the backbone (each with different finality and governance) could fragment liquidity unless common standards emerge.

- Operational concentration risk: Relying on a single ledger or a handful of custodians creates concentration risks that regulators will want mitigated.

Regulators and industry will need to resolve these issues through layered standards: technical protocols, legal frameworks and supervisory guidance.

What institutions evaluating infrastructure should do next

For fintech and institutional readers assessing tokenized asset infrastructure, practical next steps include:

- Run focused pilot programs with controlled exposures that test real collateral flows, not just token minting. Integrate custody, legal wrappers and payment rails early.

- Build or contract robust custody solutions that support regulatory reporting and key‑management best practices.

- Stress‑test liquidity scenarios with tokenized collateral in tight markets to understand operational and balance‑sheet effects.

- Engage with supervisors and industry groups to shape standards and reduce legal uncertainty.

Many firms are already experimenting; platforms such as Bitlet.app and other custody vendors are evolving products to bridge tokenized markets with regulated banking operations.

Conclusion

The ECB signalling that tokenized securities may be acceptable as collateral is an important catalyst: it accelerates the move from proof‑of‑concepts toward production plumbing where on‑chain settlement and central bank operations interact. The XRP Ledger’s characteristics — speed, low cost and deterministic finality — explain why it’s being considered as one of the practical rails. But adoption will hinge less on headlines and more on the hard work of legal integration, custody maturity and operational resilience. For institutions, the time to experiment, build governance and align with supervisors is now.

Sources

- ECB set to greenlight tokenized securities as collateral (Coinpaper)

- XRP network activity triples to ~3M (AMBCrypto)

- Market pricing and short‑term expectations for XRP (Finbold)

For wider context on tokenized assets and on‑chain settlement models, see discussions on DeFi and conventional market responses where Bitcoin remains a reference point for capital flows.